Don’t Short-Change Diversification

When we talk about diversification, the general rule is ‘not wanting all your eggs in one basket.’ Obviously, it’s important that we not be in a position to lose the whole enchilada if a company goes out of business.

But actually, diversification plays more of a role than simply protecting us from disaster. Diversification is a tool that, used properly, can improve outcomes and increase the probability that we meet our goals.

We can take a portfolio with one risky asset, say an S&P 500 fund. We can add a MORE risky asset. Maybe a fund made up of stocks of small Taiwanese companies. How does that impact our original portfolio, formerly made up of just US stocks? The answer is that, in the majority of cases, the portfolio’s risk actually goes DOWN!

The quant geeks describe this effect as follows: TWO time series (of portfolio returns) added together will have a lower standard deviation (level of volatility) than either of the individual time series IF the two portfolios are not perfectly correlated.

Put another way, the less similar the different investments in a portfolio are, the lower the likely volatility of the portfolio (and the higher the similarity, the higher the likely volatility).

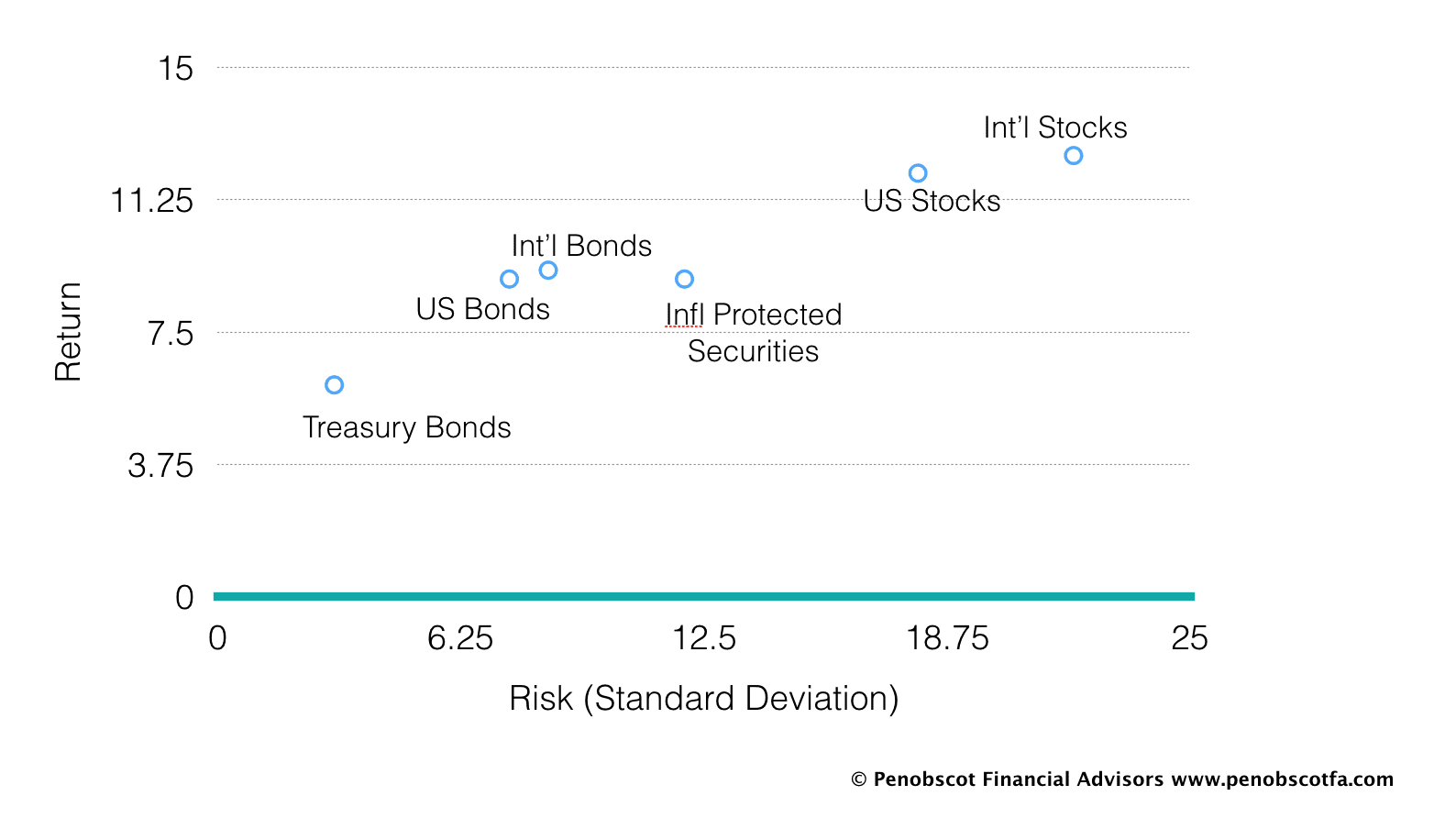

This has some interesting implications for portfolio managers and individual investors alike. Looking at the chart below, we can see that individual portfolios of various investment types have a wide range of risk/return characteristics. Treasury bills have low levels of both risk and return. US stocks run with higher levels of both risk (volatility) and return. Non-US stocks, a little higher return, and higher volatility still.

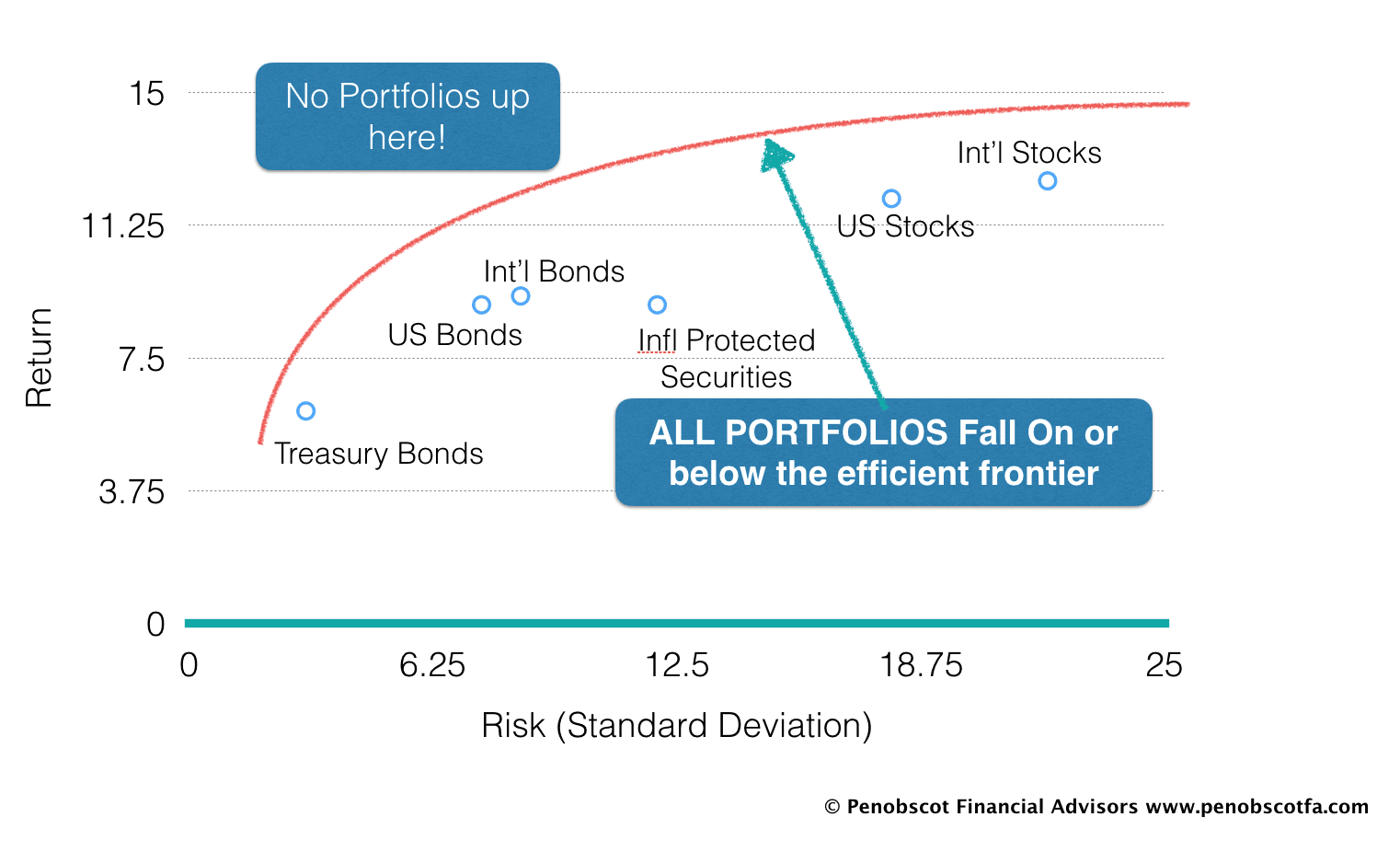

By combining different types of investments together, we can usually either increase potential return or decrease volatility – and often we can do both! But there is a LIMIT to the amount of return we can expect for any level of risk we take on. That limit is called the ‘Efficient Frontier’, and it’s the red line on the chart below.

Since we theoretically can’t invest above the efficient frontier, how can we have better outcomes from investing? One way is to add additional “Asset Classes” (categories of investments). If the asset class that gets added to the portfolio has a low enough correlation to the rest of the portfolio, the addition of the asset class will actually MOVE that efficient frontier up and to the left!

Since we theoretically can’t invest above the efficient frontier, how can we have better outcomes from investing? One way is to add additional “Asset Classes” (categories of investments). If the asset class that gets added to the portfolio has a low enough correlation to the rest of the portfolio, the addition of the asset class will actually MOVE that efficient frontier up and to the left!

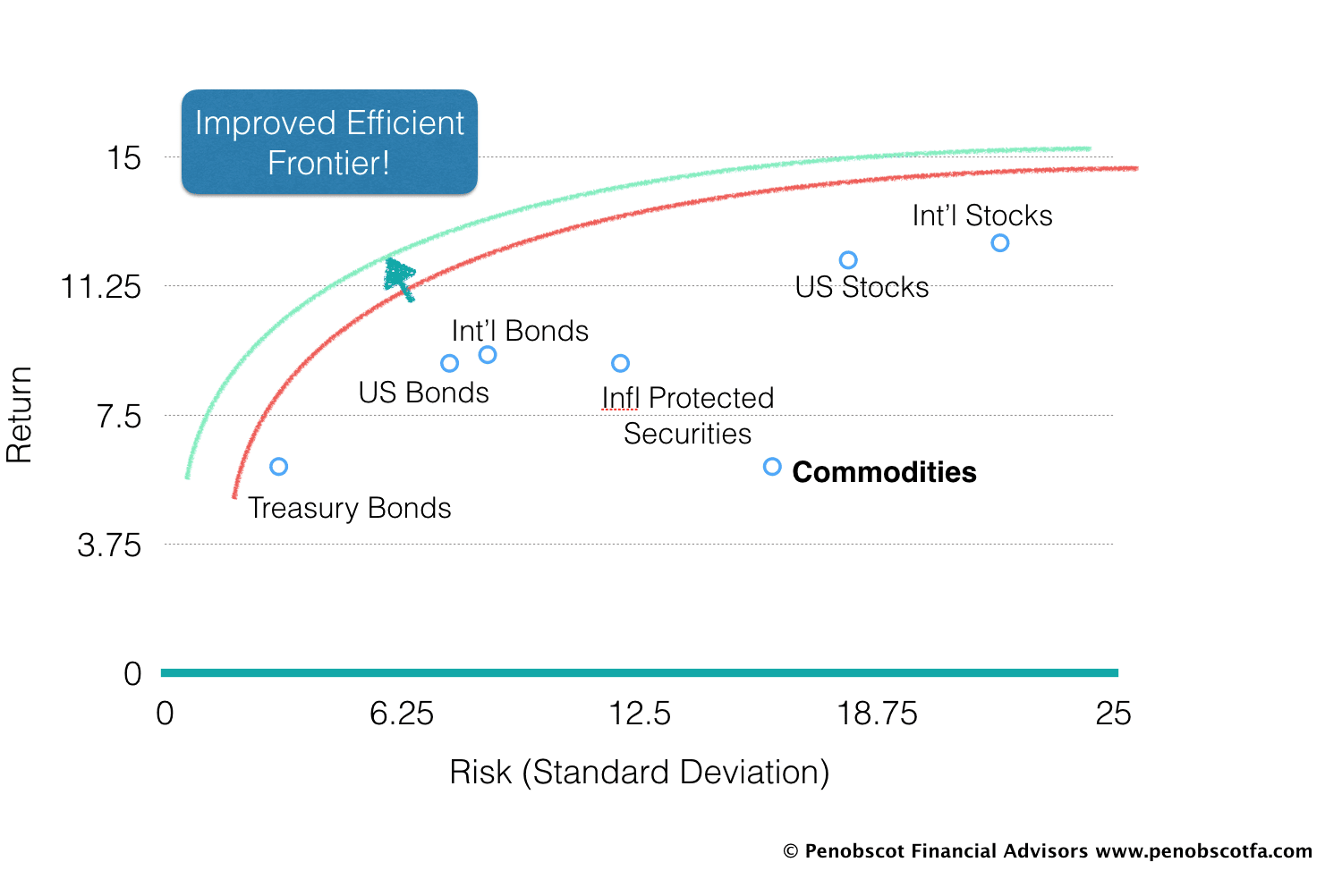

An example of this phenomenon that has been studied heavily is adding commodities to a portfolio made up solely of large US company stock. Commodities historically return less than US stocks, but their prices are still relatively volatile. The secret, though, is that price movements of commodities tend to exhibit nearly zero correlation with those of stocks. As a result, returns of portfolios of these types of stocks actually IMPROVE when we add commodities to the picture.

How can this be? Simply put, it comes down to the idea that, when comparing two portfolios with the same (arithmetic) average returns, the portfolio with lower volatility will return more, over time, than a portfolio with higher volatility. For a little more of a look into how that actually works, check out this blog post.

How can this be? Simply put, it comes down to the idea that, when comparing two portfolios with the same (arithmetic) average returns, the portfolio with lower volatility will return more, over time, than a portfolio with higher volatility. For a little more of a look into how that actually works, check out this blog post.

Diversification works. Market timing, chasing returns, Microsoft Vista… they don’t seem to work. Give diversification the respect it deserves, and it will serve you in the long run.