Improving your Credit Score

Your credit score is used by lenders to help determine the potential risk they are taking by lending you money. After-all, a loan that is not paid back is a bad investment. Credit scores do not operate like a game of golf where a lower score is better, so you’ll want to avoid that. Here is a how a lender will typically interpret your credit score:

800 – 850 is excellent, top-notch

740 – 799 is very good

670 – 739 is good

580 – 669 is fair

300 – 579 is in risky territory

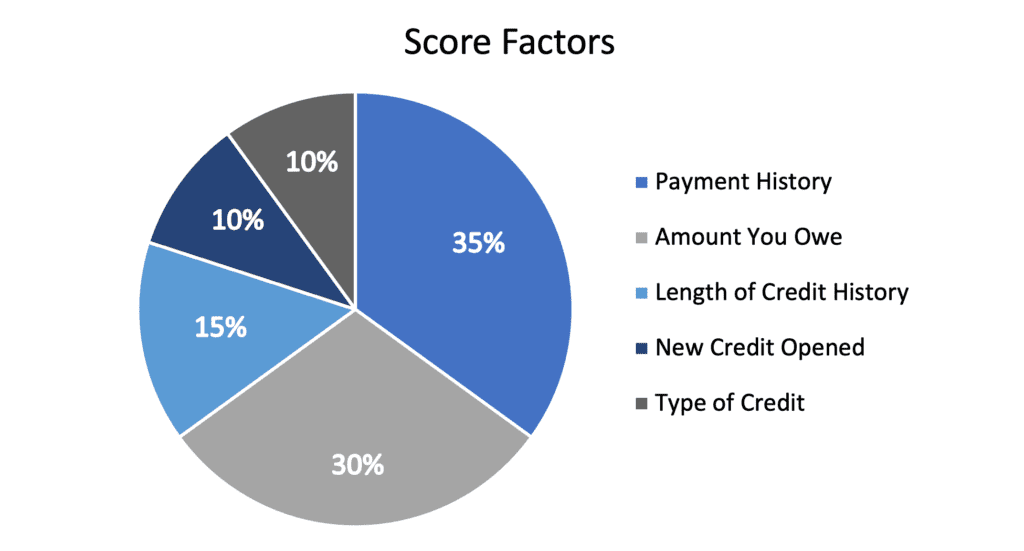

In order to improve your credit score, one must first understand how it is calculated. Your credit score is calculated based on the combination of five factors: Payment History, Amount You Owe, Length of History, New Credit Opened, and Type of Credit. Now, these factors are not weighted equally, and some have greater impacts on your overall score than others. Here is the breakdown:

Let’s look at these factors individually to identify ways you can improve your credit score.

- Payment History (35%) – Lenders want to know that if they provide you money, you are going to make good on paying back the debt. Missed or late payments reflect negatively on your score for up to 7 years from the missed payment date.

Improvement Possibility: If you believe a late payment was reported in error, you can dispute it and if it was found to be an error, have it removed.

Prevention: If you don’t have late payments, keep it up! Continue making at least the minimum payments in a timely manner on your debt. Setting up automatic payments can help take the guesswork out of “did I pay that bill this month or not?”

- Amount You Owe (30%) – When you have available credit such as a credit card, lenders want to know how reliant you are on that debt. They measure your “reliance” by dividing your balance by your available credit. When does it start to hurt your credit score? When the ratio turns out to be more than 30%. For example, if you have a credit card with a $10,000 limit, you should stay below a $3,000 balance. A helpful trick to remember this component of your score and stay below the 30% ratio is that its weight in the calculation of your score is also 30%.

Improvement Possibility: Be aware of your spending and once you reach 30% of your available credit, start using the debit card, cash, or checks to pay.

- Length of Credit History (15%) – If you went to college your parents may have recommended that you open a credit card to use for day-to-day expenses like groceries. That’s because the longer your credit history, the more positively it reflects in your credit history.

Improvement Possibility: If you are just starting out and looking to build a strong credit score, open a credit card and hold onto that sucker forever (whether you use it or not). For those looking to maintain or improve their score, hold onto your oldest line of credit even if it is paid off and you don’t use it – it will help keep your average credit age old.

- New Credit Opened (10%) – A smaller portion of your credit score but opening new credit or having too many hard credit inquiries from lenders can negatively affect your score. From the lender’s perspective, you can imagine a person opening a ton of credit cards may be doing so because they need access to the credit since they don’t have the cash currently on hand to pay their expenses – sounds risky!

Improvement Possibility: Don’t open new debt for the heck of it. Have a purpose and plan for each debt/line of credit you take out. You can also avoid too many hard inquiries on your credit during an auto or home purchase process by doing them all within a couple of weeks of one another where they may be treated as one inquiry.

- Type of Credit (10%) – Individuals can take on a variety of debts from car loans to student loans to mortgages, credit cards, and more. The types of credit you have and how many of each can tell a potential lender a great deal about how you manage credit.

Improvement Possibility: Don’t pile up only one kind of debt for multiple purposes. If you are doing home projects and have equity in your house, it may be better to use a home equity line of credit rather than putting it on a credit card, and not just because of the interest rates.

Remember, your credit score is a tool and not the end all be all. If you are looking to improve your credit score or finance a new goal in your life, you should consult your financial advisor on what strategy would be best for you and your long-term financial picture.