Opportunities that arise with market volatility

I speak with very few people who relish market volatility, and lately we’ve had more than our fair share. Of course, volatility, in general, may really not be what people hate – but rather the downside volatility. I rarely hear complaints about sharp upward movements in the market.

The fact is, however, that volatility – both upward and downward – is a necessary element in what makes long-term investing a worthwhile proposition. If markets had no volatility, shares of companies would be bid up to a point where there was very little to be made on them. Since there is, in fact, volatility, shares stay at prices low enough to make a long-term gain. For example, a savings account that returns (optimistically) 1.00% interest implies that if we want to make $1,000 per year on a savings account, we’ll need to invest 100 times that amount, or $100,000. By contrast, we often hear that the stock market is ‘expensive’ when price-to-earnings ratios exceed 20/1. But if the objective is to realize $1,000 per year in earnings on a stock trading at that very ratio, we’d only need to purchase $20,000 of that vehicle to make the same amount of earnings as the $100,000 investment in the savings account. Why? Because those earnings on the stock are not set in stone- they can go up or down from this point forward and in the meantime, markets will drive the price of the stock up and down as they figure out longer term earnings.

Investing in today’s market is fraught with a lot of uncertainty about those future earnings. As I write this, the country is largely on lockdown, transportation, entertainment and restaurant businesses are largely shuttered, and no one knows for sure how long this will continue. That’s about as much uncertainty as you’re likely to find, so determining a worthy stock price using average price-to-earnings ratios is at best like throwing a dart in the dark, and prices will likely continue to gyrate substantially as long as that future earnings number is so unknown.

Staying the course is generally advisable in markets like these, simply because we can’t know short-term market movements. Longer term, we’ve historically recovered from large economic disruptions, and there aren’t a lot of good reasons to expect this time will be any different.

But staying the course doesn’t leave you without opportunities to improve your investment portfolio. There are some opportunities that market volatility provides.

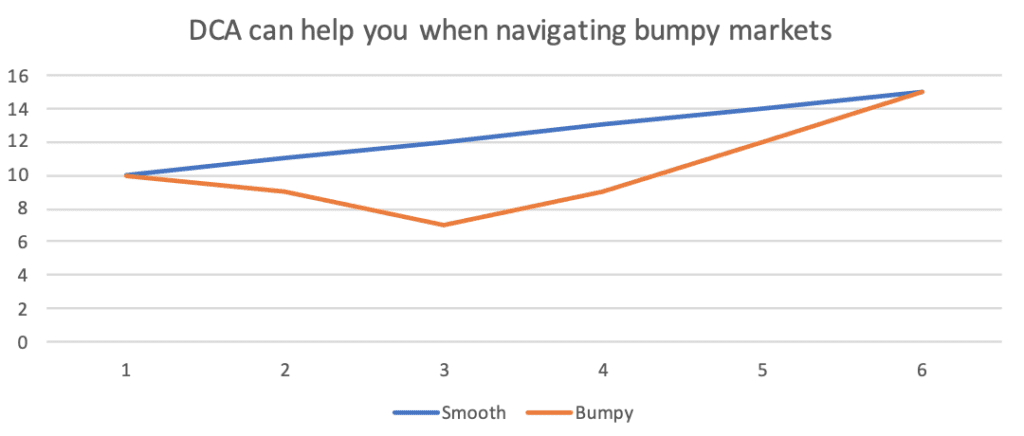

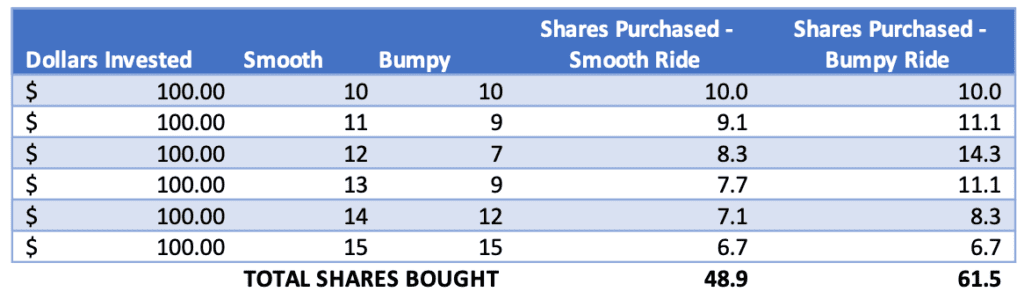

Dollar-Cost Averaging

Putting a set amount of money aside in an investment routinely is a process called Dollar-Cost-Averaging. Most people actually do this, if they have an employer plan like a 401(k) or a 403(b) where some of each paycheck goes to the investment. Assuming prices drop for a period, the same amount of money will purchase more shares than when prices go up. If prices spike upward, fewer shares are purchased when they’re more expensive.

Dollar-cost averaging can help in markets like we witness today. People who have cash to invest may not want to pick “the day” on which to get into the market. Setting a reasonable DCA schedule over a number of months can remove the emotional hurdle of getting money invested.

Dollar-cost averaging can help in markets like we witness today. People who have cash to invest may not want to pick “the day” on which to get into the market. Setting a reasonable DCA schedule over a number of months can remove the emotional hurdle of getting money invested.

Tax-Loss harvesting

During years when the market has declined, investors may have the opportunity to sell investments at a loss. Capital losses can offset capital gains, and to the degree there aren’t as many gains as losses, they can offset earned income up to $3,000 per year. Taking advantage of this may mean selling an investment you’d rather hold onto, and you can’t just sell to lock in the loss and buy the investment right back. If you repurchase the sold investment within 30 days, the ‘Wash Sale Rule’ invalidates the loss you take on the sale. Still, you don’t need to be uninvested during that time period. You can hold another investment in its place or purchase an index fund or a similar (but different) security in its place, for example.

Portfolio Rebalancing

Even if there aren’t significant losses to be harvested for tax purposes, the process of rebalancing an investment portfolio can become less of a tax headache during down periods in the market. Inevitably, rebalancing involves selling some parts of the portfolio that are larger than you want them to be and putting the proceeds into parts of the portfolio that are smaller. During long bull markets, this type of activity can generate a lot of taxable capital gains in non-tax-deferred accounts. With prices down, this can usually be done with less tax impact.

Good investors take advantage of markets like these to make their investing more efficient. They take every step possible to remove emotion from their investing. They bargain-shop, and pay close attention to the importance of how much of their gains they get to keep after they pay their taxes.