How I rescued Social Security. (And you can, too!)

Most American citizens have not experienced a society without Social Security. We take largely for granted a system that nudges over 10 million seniors above the poverty line; one that, for 1 in 4 seniors, provides 90 percent of the income they rely upon for food and shelter.

These statistics beg two questions:

QUESTION ONE: What did elderly people do before Social Security was implemented?

The visual this conjures with me comes from Willy Wonka & the Chocolate Factory: Two sets of grandparents living in one bed in the living room of their working age child. That’s probably not far off from the scene in many households. Sadly, 1 in 2 seniors was impoverished before Social Security was enacted. Those who survived to a ripe old age largely relied upon family, church, and state welfare services for their survival, or simply worked until they literally dropped.

QUESTION TWO: Knowing this, why are we allowing Social Security to become dangerously underfunded?

When I entered this field in the late 1900s, we were already aware of the fact that Social Security was going to run into financial trouble without some repairs. In the quarter century since I started, the repairs enacted have amounted to almost nothing. Outside of a couple of arguably abusive loopholes being eliminated, nothing of significance has been done.

What’s the problem?

There are lots of places to point fingers, but the biggest villain in the Social Security ‘problem’ is simple demographics.

Social Security isn’t like a 401(k). Money you put aside doesn’t go to you. Rather, it’s used to fund benefits for people currently taking distributions (Don’t worry – look at the younger people out there… they’ll be paying for your distributions someday. Hopefully.). Back in the 1930s, a lot more people were working than were eligible to collect Social Security benefits. Some estimates are that workers outnumbered Social Security recipients by 40 to 1. By the 60s, that ratio was 5-1, and was still adequate to not only pay out benefits, but to put some aside for a rainy day in what is known as the Social Security trust fund. Today, however, that worker-recipient ratio is closer to 2-1. That’s inadequate to pay out benefits… but why is this number changing? Three main reasons:

- People are living longer (apart from 2020, where the COVID pandemic actually lowered life expectancy!)

- Baby boomers have retired, and that bump in the population is no longer paying in. They’re taking out.

- People are having fewer kids. In the 60s the average family had 3.5 children – now it’s 1.8. We aren’t producing enough of those offspring to support us!

That Social Security Trust Fund is commingled with the general US treasury reserves. It is invested conservatively in special issue Government bonds. In 1983, under guidance from not-yet-Fed Chair Alan Greenspan, the fund was given a boost through tax increases that were meant to carry the fund for the next 75 years. What taxes couldn’t cover, interest income on the trust fund made up. Until it didn’t. Lower interest rates in the 2000s proved Greenspan’s scheme inadequate and last year, in 2021, the outflows finally started to exceed both taxes and interest. Now the trust fund is no longer going up in value. It’s going down. When it reaches zero, only money being paid into Social Security though payroll taxes will be available to pay out. And that’s only enough for about 80 percent of the liabilities.

Can we blame COVID, too?

It’s still to be seen, but the pandemic started out by straining the situation further. People got wildly unemployed and stopped paying payroll taxes. Then everyone got re-hired and a bunch of people, particularly older people, sadly died from the pandemic. That actually helped to slightly relieve the strain on the trust fund. But now, with the “great resignation”, we’re back to fewer people paying in. As a result, we’re circling the drain a little faster.

How can it be solved?

First, I think it’s important to say this: SOCIAL SECURITY IS FIXABLE. The shortfalls, while massive in absolute dollar terms, can be fixed with relatively mild changes. Unsurprisingly, these changes involve:

- Increasing money going into Social Security (mainly through more taxes).

- Decreasing money paid out by Social Security (carefully).

The Committee for a Responsible Federal Budget, a non-partisan, non-profit organization committed to educating the public on high-impact fiscal issues, has created a neat calculator that allows users to work out their own fixes to social security by maneuvering revenue and expense items and getting an instant look at projections that result. You can access this tool they call ‘The Reformer’ here.

After playing with The Reformer for a while, I eventually selected enough revenue and expense items to successfully get the tool to project Social Security Solvency for a 75-year period into the future and beyond. How did I do it? Here are the items I selected:

Here’s how I would rescue Social Security

- Raise benefits by 10%.

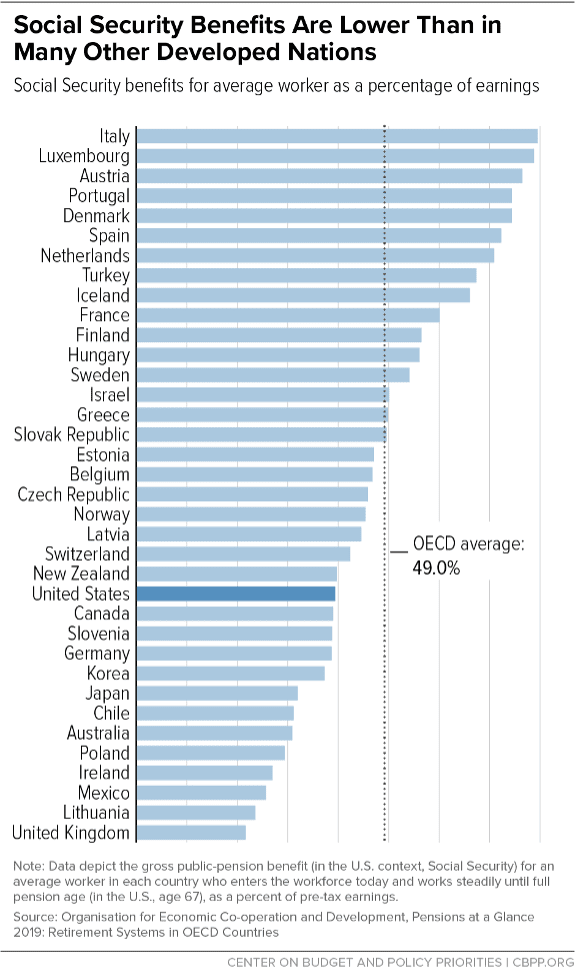

- I know what you’re thinking… Wait – I thought you were trying to SAVE Social Security! You certainly can’t raise benefits across the board and be serious about saving the system.I think that a serious reform to the system not only keeps it solvent for the foreseeable future, but also makes the US system more competitive globally. The truth is that right now, the benefits provided by Social Security as a percentage of earnings falls short of the OECD average. I feel we could do better. Also, pretty much everyone would benefit from this increase – and this could make meaningful Social Security reform a much easier pill to swallow, politically. No one gets rich on Social Security, but with an across-the-board increase to benefits, far fewer will live in poverty.

- Slow benefits for higher earners.

- Presently, the calculation of social security benefits starts with an ‘Average Indexed Monthly Earnings’ number (AIME) and takes 90% of a portion of that AIME, adds another 32% of income above that level to a point and 15% of the remainder. These ‘bend points’ in the calculation ensure that people with a lower income have a higher percentage of their income replaced by Social Security than people with higher incomes. This option would create new brackets of 90%, 30%, 10% and 5%, phased in until 2050. This would slightly reduce the percentage of income replaced for high earners but would leave intact the same benefits for the lower half of earners.[1]

- Move up the full retirement age.

- By 2027, the ‘full retirement age’ will reach 67 years of age for all recipients. Let’s face it – when Social Security was first introduced in the 1930s, life expectancy wasn’t that far ahead of the full retirement age (which was 65 years of age at the time). With increasing lifespan (except for 2020), we should accept the fact that the system is being relied on for much more income replacement than was projected at its creation. My option would be to increase the Full Retirement Age by 1 month every 2 years until it reaches 68. Workers would still be able to take reduced Social Security benefits at age 62, at a slightly larger reduction than when the Full Retirement Age was 67.

- Change to Chained CPI.

- Currently, the Social Security formula uses CPI-W to determine annual benefits increases to participants. Many argue that this overstates the actual cost of living over time, as it doesn’t account for substitution effect (for example, when the price of steak increases, more consumers will switch to chicken and thus aren’t as impacted by the price increase in steak). Chain CPI is often seen as a more accurate way of tracking true cost-of-living impacts.

- Increase the wage base to 90% of wages.

- In 2022, the Social Security Wage Base is $147,000. This means that the 12.4% tax on income (paid half by employee and half by employer – or both halves for self-employed people) applies to the first $147,000. Any income above that level is not subjected to Social Security tax[2]. Currently, this amounts to about 84 percent of wages. Increasing that base so that 90% of wages are included in the taxable base would move the needle closer to fixing Social Security for the long term and would not be a burden on most households. Higher income households would still accrue a slightly higher benefit as a result.

- Invest some of the money outside of US Government bonds.

- Fiduciary standards for investment stewards include a duty to diversify. Given the long duration of the Social Security Trust Fund, it would be prudent to widen the investment landscape. This is tricky, as it involves a lot of government investment in private industry, assuming corporate stocks and bonds would be involved. However, there should be some way of doing this in a way that is not tantamount to the government interfering in the free markets. Some global equity and fixed-income indexes would be logical vehicles, and if deployed gradually, shouldn’t impact markets significantly. It’s important to point out that volatility created in Trust Fund balances will need to be mitigated by general fund assets, which could cause annual budgeting issues. However, these issues already exist and it’s difficult to envision a scenario where this does not produce better returns over the long run.[3]

- Calculate benefits on the highest 38 years instead of 35.

- Currently, benefits are based on the 35 highest indexed years over the course of a lifetime. Realistically, though, most people work for a longer period. A change to include the 3 additional years will more likely than not result in more people having lower income (or no-income) years figured into their benefits formula. I must confess this is probably the hardest one to justify as people in certain professions (like parenting) would be more significantly impacted than others. However, lined up over a longer normal work life (remember, I’m also recommending increasing the full retirement age), it seems reasonably equitable.

- Increase payroll tax by 1.2%.

- I saved the worst for last. Yes, this would be a 0.6% increase for both employee and employer. Additionally, it would impact self-employed people more significantly. I’d love to see offsetting tax breaks elsewhere to help along self-employed individuals – perhaps an expansion of the Qualified Business Income deduction that was introduced in the 2017 Tax Cuts and Jobs Act.One important caveat: IF we were to wish to fix Social Security over the long-term, and this payroll tax increase was the only thing that was preventing its passage, the 10% increase in benefits across the board could be sacrificed. In that case, basic benefits and taxes remain unchanged.

So, that’s it. Those are my recommendations. At least they were when I went through the options available on the Reformer. The more I play with this tool, the more other options come into and fall out of my scenario. The point is, there are a huge number of ways Social Security can be shored up for generations to come. What’s important is that every year that passes without reform, these seemingly minor steps will need to become more draconian.

What if we were to put together a few of these, and take a national ballot on which combination people want? Would taking it out of the realm of elected policy makers let us collectively find the choice most people want? Seems important enough an issue to tackle. I, for one, don’t want to go back to the days of four-people-to-a-bed, hoping for a golden ticket!

[1] This exact solution was recommended by the bipartisan Simpson-Bowles fiscal Commission report in 2010.

[2] There is, additionally, a 2.9% tax for Medicare, which does not have an income cap. Medicare is in trouble, too. Maybe more so than Social Security. But that’s a topic for another blog.

[3] Don’t confuse this with an idea batted about in the 90s and 00s about privatizing Social Security and assigning people investment accounts. Solely my opinion, but that’s a horrible idea. Read Paul Krugman’s Arguing with Zombies for a number of good op-eds on the topic.