It’s also tax-GAIN harvesting season!

Okay, last week’s blog focused on harvesting capital losses, and it being a great way to reduce taxation by offsetting capital gains and, to a limited degree, regular income if done correctly.

Despite recent market volatility, though, the truth is that if you have invested over the past 10 years, you’ve probably made money in the market. This leaves many investors in a situation where they have unrealized capital gains in some of their holdings. “Capital gains” represent the difference between what someone pays for an investment and what the investment is worth today. “Unrealized” means simply that the position has not yet been sold. Since capital gains are taxed – or “realized” – only when an investment is actually sold, this leaves an incentive for holders of appreciated assets to continue to hold them, lest they be taxed on the gain.

So this week, we’ll talk about the complete opposite strategy from our tax-loss harvesting discussion last week. This week, we’re focusing on harvesting capital gains!

I know what you’re thinking: You just said that investors are incented to hold assets that have gains, lest they be taxed on the gain at the sale.

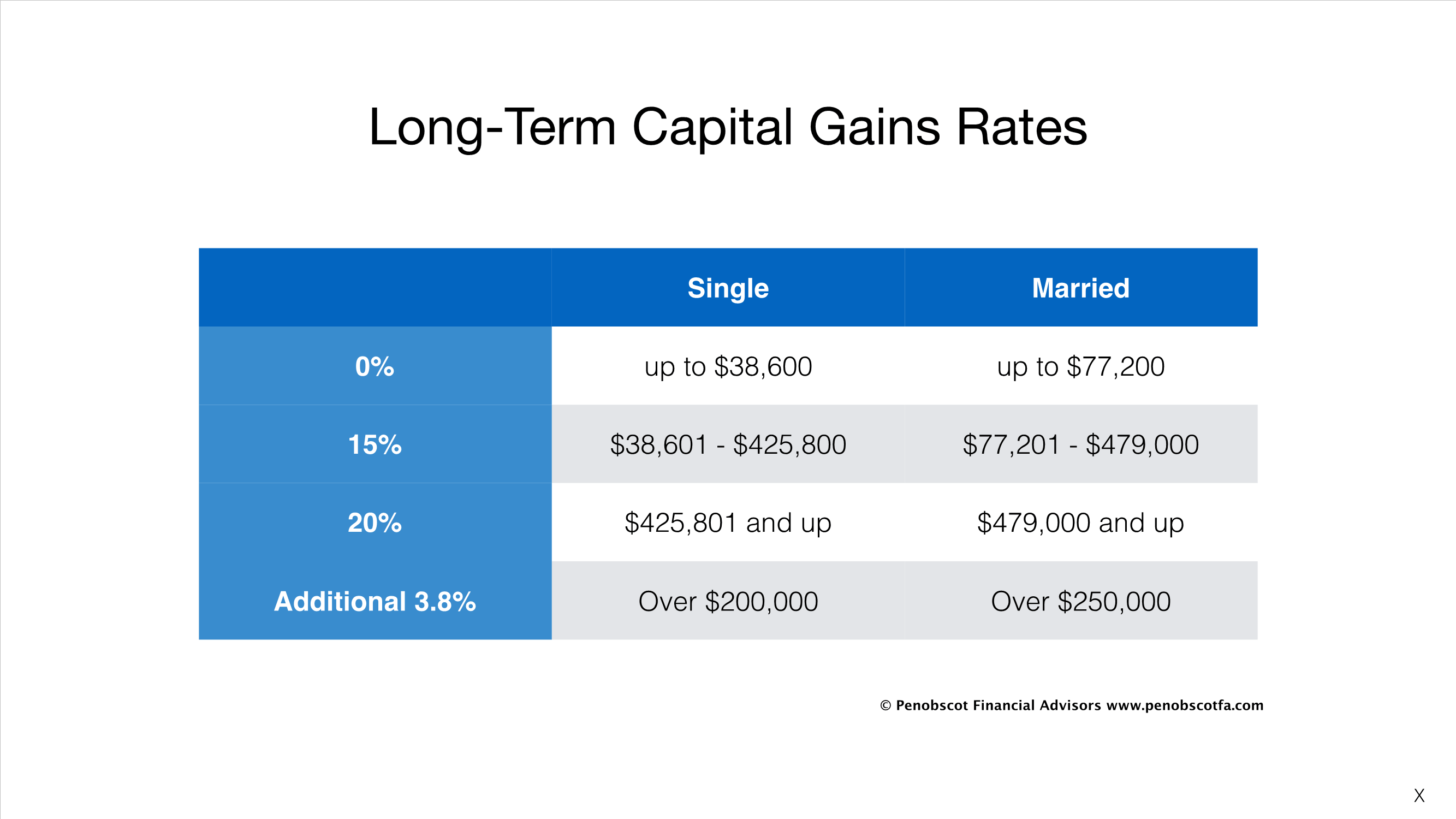

Well, here’s the rub: There’s actually a zero-percent capital gains tax rate. Looking at the chart below, the federal long-term capital gains tax rate is zero for single taxpayers with taxable income below $38,600 and married taxpayers below $77,200. This means that long-term capital gains, to the degree that they don’t push income past these numbers, escape federal taxation.

Example: Lisa and Peter are married. Lisa makes $55,000 per year on her job, and Peter makes $35,000 from his real estate business. Combined, they make $90,000. Assuming their adjusted gross income is reduced by their joint standard deduction of $24,000, their taxable income is $66,000. The amount from that $66,000 income number and the $77,200 top of the zero capital gains bracket represents $11,200 that can be ‘filled’ with realized capital gains. That much will be subject to the zero tax rate, and any realized gains beyond that will be taxed at the next brackets.

Example: Lisa and Peter are married. Lisa makes $55,000 per year on her job, and Peter makes $35,000 from his real estate business. Combined, they make $90,000. Assuming their adjusted gross income is reduced by their joint standard deduction of $24,000, their taxable income is $66,000. The amount from that $66,000 income number and the $77,200 top of the zero capital gains bracket represents $11,200 that can be ‘filled’ with realized capital gains. That much will be subject to the zero tax rate, and any realized gains beyond that will be taxed at the next brackets.

This brings up some great opportunities for tax planning. First, if an investor wants to liquidate a position and they fall into the income limitations like our couple in the example, they can do so without having to pay taxes on realized capital gains.

But even if they don’t really want to sell a holding, it may still make sense to do so. The rationale is that if a sale is made, the investment can be repurchased at the new price, leaving the holders with the same investment, but with a higher cost basis! What’s more, recall that we have to be out of a stock for at least 30 days in order to avoid the wash sale rule – but that rule does not apply to sales that happen at a gain! The stock can be repurchased immediately after the sale.

Further to the example above, Lisa and Peter have XYZ stock, which they purchased 10 years ago for $3,000. It’s done very well, and the stock is now worth $13,000. That represents a $10,000 capital gain. Lisa and Peter decide to sell the stock for $13,000 and immediately purchase it back again – for the same $13,000. Now, the cost basis in the stock and the market value are both the same – $13,000.

So, why is this a good thing? By increasing the cost basis in the stock, there will be less of a tax bite when sold in the future, even if they don’t qualify for the zero bracket.

Continuing with Lisa and Peter, next year Peter’s real estate business does very well, and he makes $100,000. Now, after including Lisa’s salary, their taxable income level puts them above that $77,200 that would otherwise qualify them for the zero federal capital gains tax treatment. They decide that they want to sell their XYZ stock and use it for a down payment on a camp. At the time they sell it, the market value has increased to $14,000. When they sell it, they’ll only owe capital gains taxes on the $1,000 in value above their new $13,000 basis. Had Lisa and Peter not had the foresight to harvest their gains last year, they would have owed taxes on $11,000, not just $1,000!

So, for taxpayers who qualify, there are good reasons to look out for opportunities to actually harvest gains. Some things must be taken into account, though, that may limit the benefit from tax-GAIN harvesting. Among them:

- It usually costs money to buy and sell stocks, so harvesting very small capital gains may not be worth it, considering trading costs.

- While the federal capital gains tax rate is zero, many states (including Maine) do not distinguish between capital gains and regular income. Lisa and Peter in the example above may very well owe state taxes when they harvest their gains, slightly reducing the benefit of doing so. Make sure you are aware of the potential increase in your state taxes.

- Other consequences might result from the realization of extra income, capital gains or otherwise. One biggie is that Social Security benefits are partially subject to federal income tax. Bigger amounts of income may increase the amount of Social Security that’s subject to tax, unwittingly causing a higher tax consequence when realizing capital gains, even if the gains themselves are at a zero tax rate.

- Some tax credits, including the Savers’ Tax Credit and the Earned Income Tax Credit, can be phased out with certain amounts of investment income. Talk to your financial advisor and your tax professional if you think you might qualify for one of these credits before realizing any capital gains.

- If you do benefit from tax-gain harvesting, make sure you don’t harvest tax-losses in the same year (you’d be using losses to offset gains that weren’t going to be taxed, anyway, and in the words of SNL’s version of George H. W. Bush, that wouldn’t be prudent.)

They’re not for everybody all the time, but for some people some of the time, both of these strategies – Tax Loss Harvesting and Tax-Gain Harvesting can put you ahead of the game and allow you to keep more of your investment returns!