Market Commentary | January 2021

Executive Summary

Market Review

2020 was a year of tremendous change and disruption. The year started with a SARS-like virus, first detected while spreading in China, being diagnosed in the US in January. February saw rapid movement in the virus taking hold, and featured political intrigue, with the impeachment of President Trump. Into March, the now-global COVID pandemic was pushing health systems across the globe to their breaking point, resulting in an unprecedented shut-down in the economy. Global equity markets dove, in many cases, the quickest they’d ever dropped. Economic activity screeched to a halt, the likes of which we’ve never seen, with the 5% decrease in the 1st quarter vastly outdone by the second quarter deceleration of over 31% and the longest period of economic expansion came to a quick halt in the US. Fear ruled the landscape as people experienced the loss of loved ones and relatives while economic hardship stoked fears of another great depression. Unemployment surged to over 15%, with north of 20 million people applying for unemployment assistance.

In April, massive monetary and fiscal stimulus programs were rolled out, with many American households getting direct cash stimulus payments and hundreds of thousands of businesses receiving pandemic assistance in the form of grants and loans. May witnessed the police killing of George Floyd and the resulting massive protests and demonstrations across the US and the globe. Meanwhile, the summer brought a downturn in COVID cases and a rapid increase in economic activity. The combination of re-openings and significant amounts of fiscal stimulus resulted in rapid improvements to the employment numbers, although they have remained at very high levels. Throughout the market bounce back, it became clear that most of the progress was being made by a relatively small number of huge companies. The market recovery largely plateaued and pulled back a bit in September, as the prospect of an emotionally charged presidential election and indications of a second wave of Coronavirus infections were poised to spoil the robust comeback.

Then came the fourth quarter, and despite the fact that the economy grew at a record pace in Q3, and many stock market indexes had regained their pre-pandemic highs, we’d argue that Q4 was when fundamental improvement really started to occur across the board. The presidential election drew record participation, despite the pandemic (or perhaps because of the pandemic) as voting became more of a ‘season’ than a date with huge numbers of people voting ahead of election day. Uncertainty about the election results gave way to more concrete indication of a mandate for change. Acknowledgement of a dark winter ahead with the new wave in virus cases was offset by hope that emerged from stellar results in vaccine efficacy and emergency approvals. A long-awaited additional financial lifeline finally began to take shape after the election and new stimulus programs were rolled out, to the tune of an additional $900 Billion, with subsequent democratic victories in Georgia (and the resulting control of congress by the democrats) being seen as a harbinger of even more financial aid to come.

While the huge names that carried markets into and through the summer continued to make progress in the fourth quarter, Q4’s bigger gains were realized by smaller companies, value stocks, and non-US, especially emerging market stocks. For managers like PFA, who routinely diversify into these areas to tamp down risk and to generate better returns, this was a welcome development. This broadening of participation in the market recovery potentially lays out a platform upon which a return to economic activity unfettered by virus mitigation measures and boosted by substantial fiscal support and accommodative interest rates, can occur. Valuations are relatively high, and risks, both political and economic still weigh on our minds, but we carry into 2021 what we feel is a justified sense of optimism.

Economic Review

Employment: Employment slowed in November with the addition of 245,000 new jobs, well below the totals for October (638,000) and September (661,000). The unemployment rate inched down 0.2 percentage point to 6.7% in November as the number of unemployed persons dipped from 11.1 million in October to 10.7 million in November. Despite the reduction in the number of unemployed persons, that figure is still 4.9 million higher than in February. In November, 21.8% of employed persons teleworked because of COVID-19, up from 21.2% in October. The labor force participation rate edged down to 61.5% in November; this is 1.9 percentage points below its February level.

Claims for unemployment insurance continued to drop in December. According to the latest weekly totals, as of December 19 there were 5,219,000 workers receiving unemployment insurance, down from the November 14 total of 6,071,000. However, data released in January saw a December reduction in payrolls of 140,000, the first monthly decline since April.

FOMC/interest rates: The Federal Open Market Committee met in December. The FOMC decided to maintain the target range for the federal funds rate at 0.00%-0.25% and expects to maintain this range for the foreseeable future until employment and inflation meet standards set by the Committee. While economic activity and employment have continued to recover, those measures remain well below their levels at the beginning of the year. The longer-range projection of the federal funds rate is 2.0%-3.0%.

GDP/Budget: In contrast to the second-quarter gross domestic product, which fell 31.4%, the third-quarter GDP shows the economy advanced at an annual rate of 33.4%, as the country continued to rebound from the economic effects of the COVID-19 virus. Consumer spending, as measured by personal consumption expenditures, increased 41.0% in the third quarter, in contrast to a 33.2% decline in the second quarter.

November saw the federal budget deficit come in at a smaller-than-expected $145.3 billion, down roughly 30% from November 2019. However, the deficit for the first two months of fiscal year 2021, at $429.3 billion, is 25% higher than the first two months of the previous fiscal year.

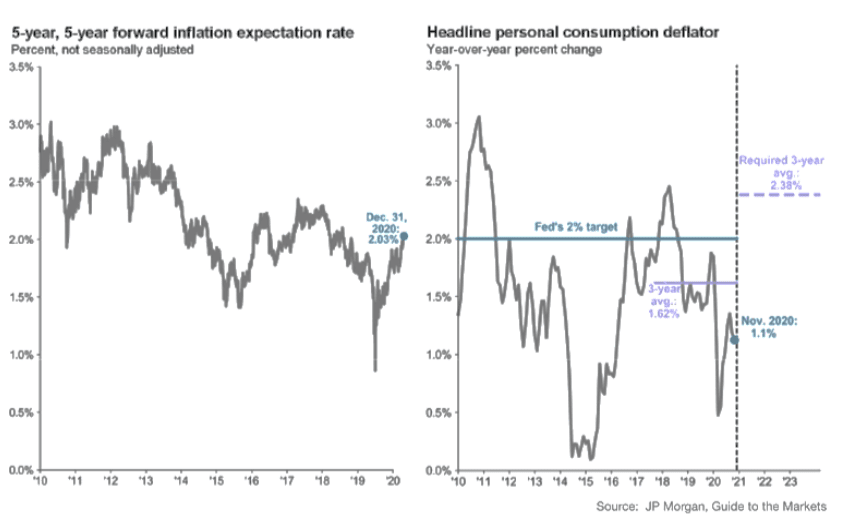

Inflation/Consumer Spending: The COVID-19 pandemic clearly impacted personal income and spending in November. According to the latest Personal Income and Outlays report, personal income and disposable personal income decreased 1.1% and 1.2%, respectively, after decreasing 0.6% and 0.7% in October. Consumer spending fell 0.4% in November after increasing 0.3% the previous month. Inflation remained muted as consumer prices were unchanged in November and October. Consumer prices have increased by a mere 1.1% over the last 12 months ended in November.

The Consumer Price Index climbed 0.2% in November after being unchanged in October. Over the 12 months ended in November, the CPI rose 1.2%. The prices for lodging away from home, household furnishings and operations, recreation, apparel, airline fares, and motor vehicle insurance increased in November. Prices for used cars and trucks, medical care, and new vehicles declined over the month. Increases in shelter and energy were major factors in the CPI increase. Core prices (less food and energy) increased 0.2% in November and are up 1.6% over the 12 months ended in November.

Housing: Sales of existing homes fell in November after advancing in each of the previous five months. Existing home sales dropped 2.5% in November but are up 25.8% from a year ago. The median existing-home price was $310,800 in November ($313,000 in October). Unsold inventory of existing homes represents a 2.3-month supply at the current sales pace, a record low. Sales of existing single-family homes fell 2.4% in November following a 4.1% jump in October. Over the last 12 months, sales of existing single-family homes are up 25.6%.

Manufacturing: Total industrial production rose 0.4% in August after increasing 3.0% in July. Although industrial production has risen in each of the past four months, it has remained 7.3% below its pre-pandemic February level.

For the seventh consecutive month, new orders for durable goods increased in November, climbing 0.9% following a 1.8% jump in October. Despite the trend of monthly increases, new orders for manufactured durable goods were 8.0% lower than a year ago. Excluding transportation, new orders increased 0.4% in November (+1.3% in October). Excluding defense, new orders increased 0.7% in November (+0.2% in October). Transportation equipment, up in six of the last seven months, led the increase, climbing 1.9% in November (+1.5% in October).

Imports and exports: Both import and export prices inched higher in November. Import prices rose 0.1% after falling 0.1% in the prior month, an increase largely driven by higher fuel prices. Import prices excluding fuel dropped 0.3% in November. Despite the recent increases, prices for imports decreased 1.0% from November 2019 to November 2020. Export prices advanced 0.2% in November after declining 0.1% in October. Overall, export prices dipped 1.3% over the past year. Agricultural export prices rose 2.2% in November, while nonagricultural prices for items such as consumer goods, automobiles, and industrial supplies and materials were unchanged, but are down 1.6% during the 12 months ended in November.

International markets: A mutant strain of COVID spread rapidly though parts of Europe late in the year, sending stocks reeling as several affected countries tightened restrictions. This latest development will likely stall what had been a recovering European economy. Industrial production and retail sales had been approaching pre-pandemic levels in several European nations. The United Kingdom and the European Union reached a trade agreement as Brexit nears its final stages. In China, the third-quarter GDP advanced 2.7% and is 4.9% higher year-over-year.

Consumer confidence: The Conference Board Consumer Confidence Index® declined in December for the third consecutive month. The index stands at 88.6, down from 92.9 in November. The Present Situation Index, based on consumers’ assessment of current business and labor market conditions, decreased sharply from 105.9 to 90.3. However, the Expectations Index — based on consumers’ short-term outlook for income, business, and labor market conditions — increased from 84.3 in November to 87.5 in December.

Looking Forward

Over our skis?

Following a remarkable year like 2020, with a record pullback in the economy, diametrically situated across from a very solid return in stocks, the obvious question is: has the stock market recovered too quickly and too far? Are we in a bubble, the likes of which we saw in early 2000 – and should we be worried about a really substantial movement down?

This possibility can’t be dismissed out-of-hand. Prices, relative to earnings, are at a level we haven’t seen since the ‘irrational exuberance’ we saw in 2000. The pandemic that shut down our economy earlier this year is still raging, claiming more lives than ever. The political discourse in our country is fraught with divides between and within the major parties. The incoming Biden administration has indicated that higher taxes on corporations and wealthy individuals very well may be part of their policy platform. The significant increase in US debt, which is now higher than the Gross Domestic Product, bears out some assuredness that regardless of who is in power, some degree of increased taxation and the resulting headwind to economic growth is inevitable.

Creating further challenges, bond yields are so low that safe havens are yielding negative real (inflation-adjusted) returns. Commodities, long seen as a hedge against inflation and stock market volatility, have been growing more correlated with stock movements in the recent decades.

While all of this creates challenges and does capture our attention, we still need to invest our clients’ assets in a way that responsibly balances the risks we face currently with opportunities that exist. And we feel that, in the upcoming year, there are plenty of reasons to maintain some optimism.

High Prices in Context

One factor in our willingness to accept some justification in current price levels is the low interest rate environment. This is a significant distinction from the asset bubble we saw in the year 2000. At that time, price-to-earnings ratios on the S&P 500 exceeded 25. Paying $25 for one dollar of earnings implies a 4% earnings yield. In the spring of 2000, the 10-year treasury was yielding over 6%. With current price-to-earnings ratios over 30, the S&P earnings yield is only a bit over 3%, but this still exceeds the 10-year treasury yield by over 2%. Simply put, higher price-to-earnings ratios are generally considered acceptable in lower interest rate environments.

Lower yields longer

Lower rates are likely to remain in place for the foreseeable future. Even if inflation picks up, it would need to stay significantly higher for a long period to exceed the Federal Reserve’s target of 2% average.

Improvement is broadening

While most of the recovery in the summer months was driven by a handful of mega-cap technology companies, more recent improvement has been seen with smaller companies, such as those that make up the Russell 2000 index. By year-end, the small cap stocks had closed the gap with the bigger firms that make up the S&P 500.

Yield curve points to continued expansion?

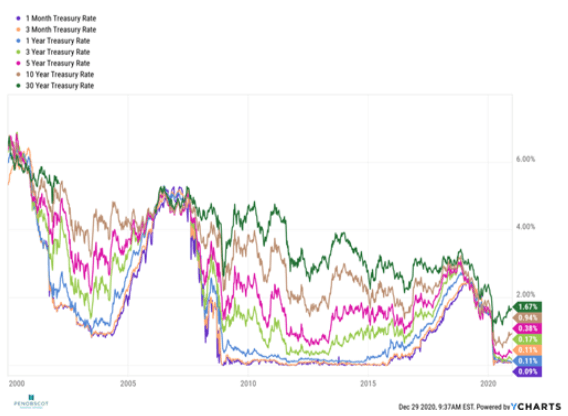

Although nominal yields are low, the spread between the short and longer-term bond yields is widening, and not compressed like they typically are ahead of recessionary periods.

Fuel in the tank

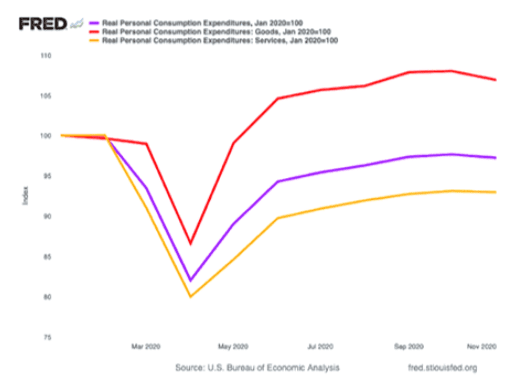

While spending on goods has actually surpassed pre-pandemic levels, spending on services is still lower and represents an area of potentially pent-up demand.

More opportunity abroad

While US stocks have recovered and are at arguably extended price-to-earnings ratios, stocks abroad show similar rebound potential, but may have further to go in their recovery.

This is especially the case with Emerging Market stocks. Some economists think EM stocks are poised to significantly outpace US stocks as historical relationships revert to the mean.

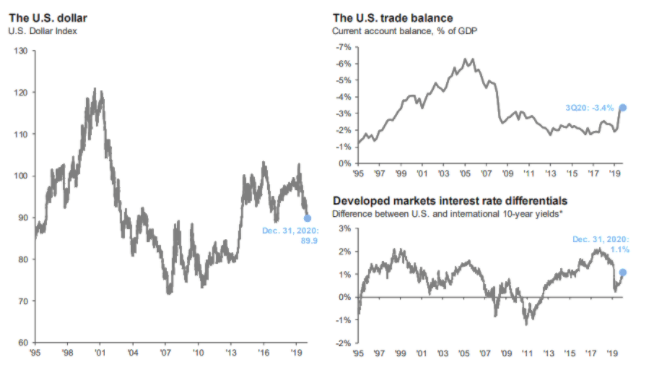

Instrumental to all of this is a dollar that has been weakening relative to foreign currencies and which may continue to do so. An increasing trade deficit (which results in more dollars flooding the world economy) and a reduction in US interest rate advantages could cause this weakening of the dollar to continue for some time.

We are pushing forward, therefore, with cautious optimism. While attempting to avoid areas of the market we see as ‘over-bought’, we continue to find cases where earnings and prices are running at attractive levels. This applies not only to stocks, but to credit investments where we see above average risk and below average return potential. We will continue to seek out innovative ways of reducing risk in our portfolios, using alternative assets where necessary in order to find lower levels of correlation. In the 4th quarter of 2020, we’ve added some exposure to areas most devastated by the pandemic in order to be best positioned for what we see as an inevitable run on services in the second half of 2021.

DISCLAIMER: The foregoing content reflects the opinions of Penobscot Financial Advisors and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Transcription

Sam: Okay. Hello everybody and welcome. Thanks for joining us today for another edition of the PFA Investment Update. We’re looking out from quarter one of 2021 now. The date today is January 29th. I am joined by our guest and Founder and Chief Investment Officer and many other things, James Bradley.

Jim: Hi, Sam.

Sam: Hi Jim. How are you doing today?

Jim: Doing great. How are you?

Sam: 2021 treating you well? Everything back to normal?

Jim: So far so good. Not quite what we’d call normal yet though, is it?

Sam: Time to find out how quick we can get there. So we’re going to follow the same agenda we followed last quarter if you joined us where we’ll take a look at the economic review, bit of market review, and then looking forward. There’s also a PDF version of this you’ll be able to find on our website. Digs a little deeper into the different aspects of the economy and some other good details in there if you’re interested. But with no further ado, let’s kick off with the economic review.

I’m going to kick us off here with talking a little bit about GDP. This was as of December 31st. So this didn’t include the most recent GDP number, which just came out yesterday. But looking back, we can see that 5% contraction in the first quarter, 31% contraction in the second quarter followed by a rebound of 33.4%, and then this last quarter came out at a much tamer 4%. Also interesting to look at the components of GDP there. We can see that housing has been a strong pillar of GDP over the last year. Consumption has actually took a dip at first, but has rebounded and remained pretty steady. We’ll talk a little bit later on about how some of that consumption has shifted though from services to goods and government spending had obviously increased a bit to plug the gap in consumption that we saw immediately following the shutdowns.

On the next page here, this is an updated chart that includes the fourth quarter, although you can barely see it after the big swings we had in the previous. There’s that 4% and the headline really says it all here with U.S. economic activity increased at a 4% annualized pace in October through December. For the full year, the economy contracted at 3.5% annualized rate, for the worst since 1946. So we’re going to look back and see if this is a 1946 situation. Many people think not. This was more of a self-imposed recession that we brought upon ourselves and hopefully that creates an opportunity for us to bounce back from it pretty quickly. So far that has been the case.

Moving on here we can talk a little bit about global GDP. So this is a chart from the IMF that shows how segments of the global economy are expected to perform versus their pre-COVID trends. Those dotted lines there would be the pre-COVID trends, the chart’s index based off the 100 line there, which would represent GDP from the fourth quarter of 2019. So anything above that, you’ll get to 105, that means you’ve grown 5% since then. So you can see the trend lines there. One you’ll notice first off is the red line there, which is China. They had a pretty good GDP trend going on prior to COVID. That makes it a little easier for them to dig themselves out of a hole. Also, they were able to take a hit by the virus earlier and were able to use the more draconian methods we could say to stomp out the virus. So they are expected to bounce back the fastest out of all these. They’ve really reached back to that trend line already and are expected to, looks like, stay pretty well in line there.

The yellow line represents the emerging market economies of the world, excluding China, which is now debatably an emerging market economy. And they are expected to reach 2019 levels of GDP by mid-2021. Down bottom on the blue line, you’ll see that world advanced economies, which are expected to return to 2019 levels of GDP by the end of 2021. But we can see based on those trend lines that still be a little catching up to do to get back to the trend we were on before COVID hit, but clawing back quite a bit so far. Kick it over to Jim, talk a little bit about unemployment.

Jim: Unemployment, and what a huge swing we saw. I don’t have the numbers exactly, but I believe what I heard was within just a couple of months time we saw both a record, an 80 year low in unemployment and an 80 year high in unemployment in that same period. Now the good news is it’s obviously come down and come down to a greater degree, I think, than a lot of economists had predicted. A lot of the ones that we follow were predicting double digit inflation to start out 2021 and that’s certainly not what we’re seeing. We see that the overall unemployment rate has come down and ended the year at about 6.7%. US initial jobless claims came down obviously pretty steeply as the summer went along. They’re still elevated and obviously still a concern.

Jim: But I think a greater concern is the first thing we were talking about, the unemployment rate certainly down, but visibly plateauing. So we’re hoping for some improvements to be seen as we actually get to reopen larger segments of the economy. That’s resulted in a lot of government borrowing and the gross federal debt as a result has increased pretty substantially. And this chart here looking from 1940 to the present, we can see that for the first time since World War II we’re over 100% of GDP as our debt, which is something that we should probably be a little bit concerned about. We could dedicate an entire podcast on just that one topic of whether too much debt is still a bad thing or whether it’s a necessary thing. It’s definitely resulted in a more significant comeback. A lot of that debt has to do with fiscal and monetary policy positions that the fed and our government has taken and global governments for that matter to plug the gaps that are recreated by the lockdowns that we saw earlier in the year.

And that’s resulted in a big increase in the amount of money that’s available out in the economy right now. If we look at M2 money and what M2 money is, is simply … well in order to understand M2 money, M1 money is the money you’ve got in your pocket plus what you’ve got in your checking account. And then to get to M2 take that and add on your savings accounts and money market funds and some short-term time deposits like short-term CDs and that’s the M2 money supply. And so to see historically that amount kind of grow gradually and then the big bump that we’ve gotten lately just says a lot about what you need to know about what’s out there as far as money sitting on the sidelines, waiting both in consumer bank accounts and in corporate reserves to really be able to deploy when the all clear happens and we can actually do that.

Interestingly 20% of all the money that was created in the United States over time was created in 2020. So one out of $5 ever created by our government was created this past year. Having that big amount of debt is troublesome, especially if it gets expensive to pay it off. So one of the things we’re definitely looking at is interest rates. Are they going to stay low and did they stay low for a long enough period of time? There’s an arguable situation that results in potentially us being able to grow our way out of the deficits that this has created. And there’s a lot of reason to expect that rates will stay low for a longer period of time. The fed participants are pretty much unanimous going through to 2022 and really almost unanimous going even through 2023 on likely staying low and the current interest rate levels, even if it makes for an increase in inflation.

And that’s one thing that we’re always concerned about. If you get too much money printed, too much money out there chasing a set amount of goods and services, money stays cheap because of the fact that interest rates are low. Historically the big concern around that is inflation. The conventional wisdom is that what we’re seeing right now should result in pretty significant inflation, but that was also conventional wisdom back in the global financial crisis of 2007, 2008. It really didn’t turn out that way. So in search of new explanations for what’s going on, some have turned to things like modern monetary theory, which takes into account differential over time between what you might expect from an inflation standpoint and what you actually get. And they explain it away by maybe we’re not seeing inflation because our economy is a supplier of a reserve currency or another alternative reason is that especially with a lot of the advancements being made in technology lately, they result in increased worker productivity, increased worker productivity increases output, and that just creates more goods and services.

And so the concern is that we’ve got a set amount of dollars chasing a set amount of goods and services if we increase those dollars. As long as we increase the goods and services that they’re chasing it maybe doesn’t get so inflationary. We also think that that is likely to stay a little bit stayed even if inflation does pick up because it can run a little bit hot for a period of time without exceeding the 2% average kind of symmetrically over a long period of time of being below the 2% we might be able to tolerate a little bit of that higher inflation into the future. One other factor that we are looking at a lot is, especially when trying to determine where there’s opportunities, is in the dollar. Is the dollar weakening or getting stronger? Right now we see a weakening dollar.

Is that a trend that can continue? We argue that it could. Two big factors. There are the trade deficit and the box to the upper right that you see there is an increasing trade deficit. Any trade deficit just simply means we’re buying more foreign goods than we’re exporting. That means we’re flooding the global economy with dollars and flooding global economy with anything is going to make the price of that thing go down. So it’s dollars, dollar weekends in that particular case. Also differentials between our 10 year yields and those of other developed markets. If that difference is closing and it seems to be doing so right now because our interest rates are being lowered while countries like Europe are trying to actually crawl back out of their sub-zero rates. That can also hold back the dollar and cause more dollar declines. So for those reasons we’re being careful in the inflationary environment. Then we’re also looking for opportunities to take advantage of tailwinds caused by a declining dollar.

Sam: Those two factors, whether inflation shows up and the direction of the dollar, very big factors in what happens in the market in the coming few years. So that wraps up the economic commentary. We’re going to move into a little bit of market review. Kickoff to answer my mother’s monthly question of is the market going to crash? Tell her that, “I don’t know and anybody that [inaudible 00:12:28] sell you something.”

Jim: Exactly.

Sam: But looking at the PE ratio here for PE ratio compared to the historical averages in the S&P is looking pretty high by that yardstick. This table here, you’ll see on the graph also provides some different valuation measures that you can use to gauge whether the S&P is overvalued or not. Cape ratio we’ll talk about on the next slide, but you can see dividend yield at the moment’s around 1.59%, 25 average about 2%. So prices would have to come down a little bit to match that 25 year average. The one metric on here that says the stock market is not overvalued [inaudible 00:13:10] the S&P at least is the spreads between earnings yields and moderate risk bonds, BAA yield bonds. So what that’s looking at is how much more is a stock earning you in yield?

Sam: And you can think of that as just the flip side of the PE ratio. Call it the EP ratio of how much are you yielding based on the price and earnings difference between that and what you would yield on a medium risk bond is actually wider now than it has been on average, which actually makes stocks very attractive relative to bonds. That’s largely a function of the low interest rates at the moment, but has kind of affected market behavior quite a bit where going to bonds at this point is taking a lot of risk off the table. There’s not a whole lot of return generation happening there at the moment with interest rates where they’re at. So we’ve seen a lot of the corrections in the market happen kind of within the equity asset class where you’ve seen a lot of shifting between like the safe stay at home stocks on the more defensive tilt versus the cyclically sensitive stocks on the other side that are banking on a come back in the economy.

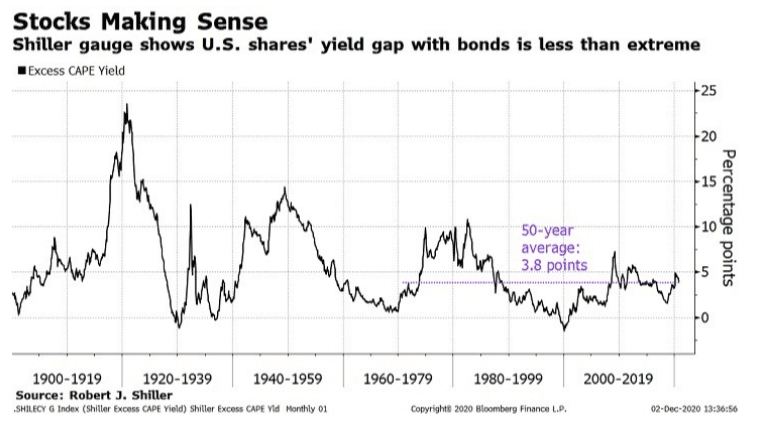

So that’s been an interesting factor that we haven’t seen the huge flows into risk off assets like fixed income as much as we’ve seen in the past. But we’ll give you a few reasons here that sometimes it is okay for the averages to be above their long runs. So we talked briefly about the Cape ratio. What that is is cyclically adjusted price to earnings ratio. So as I said, there are certain times where PE ratios should be higher than the long run averages. Things like low interest rates and low inflation expectations should push PE ratios higher. So what this is is a system created Robert Shiller who’s a Nobel winning American economist that adjusts for where you are in the business cycle, talks about where inflation’s at and where it’s expected to be, where interest rates are at.

And you can see by that measure, we are reaching that just about overvalue territory in the S&P 500, but pales in comparison to where we were in the .com bubble. People try to draw a lot of parallels right now to the .com bubble. And by this measure, you would say that that’s not a fair comparison. We’re not nearly at those levels of overvalued stocks in the S&P. Another thing we’d like to show you here is just the dispersion of equity valuations within the S&P. So those top 10 stocks are trading at about 33 times earnings versus the 19 average where the remaining stocks are only trading at 19 versus the S&P long run average of 16.

Some stocks looking pretty expensive, but some of that can be justified as well. You look at Microsoft, just produced their 14th consecutive quarter of double digit revenue growth and Apple just blew out earnings again. Some companies of size that we’ve not seen in the long run averages that are still growing pretty quickly. Elsewhere in this chart you can see that those top 10 stocks are now weighted heavier than they have been at least since 2000. And that since S&P is market cap weighted, they produce a more dominant effect on the index overall.

Jim: Just like you say, it’s a little bit less concerning when you also see that these big companies are also generating a lot of the earnings that are going into it. Kind of justifies them moving the market a little bit more, but you’re right. There’s a lot of areas in the market that haven’t had that kind of eye-popping performance, certainly online retail, information technology, and home improvement. Those are areas that have really done well, but there’s plenty of obvious industries that have a long way to bounce back. Airlines and real estate investment and cruise lines and hotels and that type of thing, and energy stocks, all are still significantly down from where they started the year.

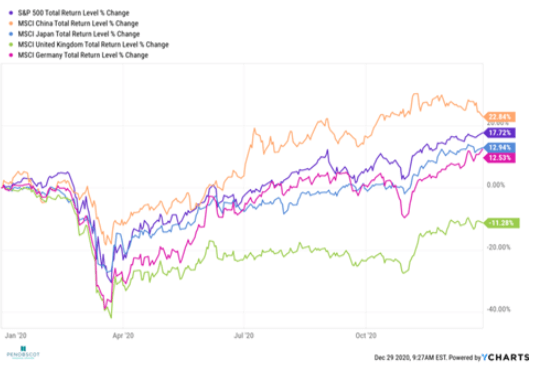

Sam: Absolutely. Definitely some value opportunities, even if the S&P as a whole is looking pretty expensive. Zooming out a little bit because it’s the other thing to be reminded of is the S&P 500 is not the entire stock market. There are a lot of other companies out there that are not included and big ones in there would be the mid and small sized companies. The S&P only factors large size companies. And while those large companies were out performing earlier in the year, really coming out of the bottom of the Coronavirus, it was a strong get stronger environmental of those large companies had stronger balance sheets and cash flows. They have lower cost of capital and often able to grab market share from smaller companies that were failing. However, with positive vaccine news in the fourth quarter, we really saw a huge fourth quarter come back by the smaller and mid cap companies that were more sensitive to the virus impact is people who became more optimistic.

And if you zoom this chart out further you would see that mid and small cap companies actually underperformed the large caps in the last market cycle, which is atypical. Smaller companies typically carry higher risk, which correlates to higher returns over the long run. For this reason, we think that small and mid companies still have some room to run, both due to the tailwinds of economic reopening as well as just those differences in valuations that have resulted from that underperformance that have them looking a little cheaper. Zooming out even further because the US is not the only place you can invest. It’s easy to forget that over the past few years as US is-

Jim: Mm-hmm

Sam: International counterparts, but I have friends that say, “I’m not investing in anything because US is printing so much money and interest rates are so low and stuff.”

Sam: I have to remind them there’s a few other countries out there you could-

Jim: there actually are.

Sam: In the teal we have the USA index as defined by MSEI. The dark blue would be the developed world. So advanced economies excluding the US. And then the green line would be the emerging markets economies. Similar to how we saw, the small and mid caps rally in the fourth quarter. We saw that the [inaudible 00:19:05] markets as well. They get a few tailwinds going between the low interest rates, the dollar weakening is also very positive for a lot of these countries that are other money in USD because their local currencies are too volatile so now they’re paying back their debt dollars that are cheaper than they were then they borrowed. Low oil prices are also positive for emerging markets and we weren’t sure how they were going to fare with the virus, but it turned out they actually fared pretty well relative to the developed world. So it’s been a strong quarter for them and also something we expect to continue. Flipping over to Jim for a little fixed income update.

Jim: This chart that we’re looking at right now is a pretty busy looking chart, but what it simply is, is just the range of treasury rates from really short term stuff, one month stuff, all the way up to 30 year stuff and going back to the year 2000. What I look at pretty closely here is not necessarily the absolute level, but the relative level between the treasury rates. So you see, we started in 2000. They’re all kind of bunched together. Same thing was true back in 2006, 2007. Same thing was true back in 2019. And that bunching together tends to represent a flatter yield curve and the flatter yield curve just tends to be something that a lot of economists look at as heralding a recession. Certainly in those situations it did. So one thing that’s interesting to look at is that now, although rates are still low, we have seen a widening out of that yield curve.

And there’s a little bit broader of a range there. Still, at the end of the day, yields are low on fixed income. And so the question is where can we get returns and how much risk do we have to take on to get the returns that we’re looking for? And there’s a pretty wide range out there, but this chart definitely kind of helps us to kind of put into perspective some things that are riskier also give us better returns. It’s a matter of is it worth the additional amount of risk? And so going into high yields and senior loans, emerging market debts, and that type of thing, may not be such a bad place to be for parts of the fixed income allocation still today. They’re certainly getting a lot of support from the fed and it’s really kind of a bleak environment for picking up yields.

So if one can do so and take on not an undue amount of risk, that can help and when we’re shopping around for overall yields. Bankruptcies are not a big, big concern right now and that’s kind of surprising to us. We’d expect, given the unemployment rate, to see business bankruptcies and personal bankruptcies at a much higher level than they are right now. Certainly relative to the end of 2019, relative to the global financial crisis, relative to where we’d expect them to be. They’re low right now and that’s not just in the United States, but globally bankruptcies that we look at this chart as that blue line of the great lockdown is showing us in a situation where bankruptcies have actually come down globally.

Largely because again, this was a manmade economic slowdown that countries pretty much across the globe were able to kind of plan for a little bit and have fiscal and monetary rescue tools at the ready to stave off bankruptcy. So hopefully we stay with that kind of a trend and that as we climb out of this and these fiscal and monetary aids start to kind of bleed off, we don’t see a pick-up. And if that all happens well, then taking out a little bit of fixed-income risk could be justified right now.

Sam:

Excellent. Thanks, Jim. So that wraps up our market review. Talk a little bit about the equity and fixed income markets. Now we’re going to look into some of the things we’re looking at going forward. No big surprises here. Looking at the vaccine rollout, how effective that is, and how quickly we can move towards herd immunity and also how consumer behavior is going to change after all this is said and done. There some trends that’ll be transitory and end after Coronavirus, but there’ll be some things that will create structural changes in the way that people behave and spend their money. So trying to separate the signal from the noise there will be very important as well to see what’s going to stick. Talking about vaccine rollout. Here’s a chart on vaccine doses administered per day between December 26 and January 19th. You see we get over a million there quite briefly. President Biden’s committed to administering 100 million doses within his first 100 days.

Since the 19th I think we have been over that million doses a day mark. So that’s positive news. But remains to be seen if the supply chain can keep up with that level of production to keep getting those vaccines into people’s hands and bodies. So Moderna and Pfizer are estimating that 70% of the population can be inoculated by July. It’s unclear exactly what percentage that we need to hit to reach herd immunity. Differs with every virus. Latest estimate by Dr. Fauci, which has been coming up, started out at 70, but now it’s up to 70 to 85% to reach herd immunity.

Right now I think we’re between five and 6%, but things are scaling up. So don’t want to say that the end is near because I think we’ve all felt that way for awhile, but certainly nearer than it was a few months ago before the vaccines were in the picture. Here we can see how the US stacks up versus some of the international countries here. Really in the middle of the pack on this chart. Vaccinations per 100 people during the short time period of January 20th to 24th. We’re 6.2 in the US for every 100 people were receiving at least one dose of vaccination.

Jim: So right, getting onto backgrounds of the kind of economic view of what the COVID recovery looks like. Our friends at Vanguard provide us with these estimates as to what are we trending toward and we’ve got an optimistic versus a pessimistic view of things. How we actually get back to our pre-COVID-19 trend on our economic growth. And based upon this, they’re saying by the end of about 2022 and their base case scenario, we get there. We could get there earlier if we have some upside surprise and it might take longer if we have some downside surprise. Their explanation of upside and downside is on this next little graph here. They are pretty comfortable with their base case or upside surprise scenarios, those making up about 90% of the probability that they’re looking at and they’re basing it on immunity gap, they call. How far the major economies come in getting that herd immunity in place, the reluctance gap, in other words.

The amount of reluctance that people have in jumping back into the economy and how quickly they do it and its results on the economic recovery. Clearly, it’s going to impact different sectors differently. What they call face to face criteria, whether it’s low, medium, or high. It’s not terribly surprising that lower face-to-face sectors like IT and that type of thing don’t require that much time to come back in this kind of a pandemic, whereas the higher face-to-face sectors, not surprisingly retail, transportation, arts and entertainment, and everything are going to take a bit longer. Anybody who’s never tried to kind of do a virtual cruise will realize that’s not really the thing that people are going for and they need the real thing, but does require a lot of higher face-to-face involvement there. So we need to be probably a little bit realistic and knowing that, yeah, those will come back and they should come back relatively strongly, but it will take a while beyond some of the other sectors and those.

Sam: Definitely interesting to see the percentages of GDP there were low face-to-face sectors actually representing 70% of GDP. Now it’d be interesting to see how that’s changed over the years, but that was higher than I would have expected.

Jim: Right.

Sam: But in the same vein, this chart here is going to show a little bit about the consumption we looked at early on as 60 something percent of GDP personal consumption here and how it’s changed. You can see on net, it hasn’t changed that much, but the differences between goods and services has changed quite a bit. So if you were going out to restaurants before, that was a service, but now you’re buying your groceries from the store, that’s a good and there’s been quite a shift there from services to goods. We get to imagine that after all is said and done here, when we do reach herd immunity and the doors are reopened, that there will be a run on services. I know I could use a vacation. I’m sure a lot of people could.

Jim: Absolutely.

Sam: But a lot of those more face-to-face service sectors should have some room to keep growing and they haven’t. They’re on that lower end of the PE spectrum at the moment. We’ve seen some rotation in the market out of the top 10 there into some of these smaller service stocks and we expect that can continue over the coming months as the pandemic proceeds a bit. And a little bit along the same lines here, here’s some high-frequency data. I think we looked at this in the last quarter. So just an update here on some of these different service sectors and how much they’ve been hit so far. [Inaudible 00:29:29] bounding things like seated diners were down 100% and now down 64%, TSA traveler traffic was down 96% now down 55. So as I was talking about consumer before the trickier [inaudible 00:29:45] how much we returned to the pre-pandemic trends versus what’s actually structurally changed within the economy.

Sam: Airlines, for example. Like I said, a lot of us will be go out there, be a big run on services as we want to take a vacation. However, there are different factors to think about like business travel. Business travel is a huge portion of airline revenue and our business is going to go back to sending their people across the country every week, or it’d be with people gotten pretty comfortable with the Zoom calls. That’ll be interesting to see. The work from home trend is another one that’ll be interesting to see how much of that sticks, how many people go back to the office. As you’ve all noticed. I’m sure when you’re working from home, your spending habits do change. You might not be going out to lunch as much. You might not be paying as much for gas and that money is spent elsewhere.

So that is separating the signal from the noise after the pandemic. It’s going to be a lot of very interesting economic studies done I’m sure in the coming years on behavior during this period.

Jim: No doubt. No doubt. Speaking of behavior, huh?

Sam: Oh yeah. There’s one thing that originally weren’t going to put in here. We’re going to wrap up at that moment, but it’s been grabbing so much headlines lately that we figured we’d touch on it and that’s the rise of these meme stocks, GameStop being the most prominent. Also ones like AMC. Companies that you wouldn’t think would have 1000 1700% returns going on before the pandemic and especially after. A lot of these companies were struggling before the pandemic and I’m sure a lot more of you now know what a short squeeze is then knew about a week or two ago. I just can’t believe how even going through Instagram, everybody’s talking about short squeezes.

It’s very strange. But it’s just a new market phenomenon happening resulting from a bunch of individual investors on internet chat boards, pooling their money together, and then going really hard into these stocks. And part of the explanation is they’re not necessarily going into these stocks because they think they’re undervalued and should be valued higher. I don’t think a lot of people truly believe that about GameStop and AMC, but these companies have a ton of short interest in it and what that means is a lot of people betting against the price. And if you’re betting against the price, you’re shorting the stock. So you can think of that as you have negative one share of stock and to close out your position, you got to buy a share of stock to get back to zero. And that’s something that continues to drive up the price.

So these people want to continue taking their losses. They don’t have to buy the stock back, but if you’re in a short position and you want to close out the position, you get to buy the stock, which drives the price up even further. So a lot of the money is just being pooled into these stocks to create the short squeezes and it’s caused some pretty wacky market activity over the past few weeks. A lot of these companies, we talked about the very low interest rates previously and one of the concerns when interest rates are very low for very long, that you can create zombie companies, which is just a company that doesn’t really deserve to exist from a hard line free market approach. You would say that a recession should shake out any weakness in the companies. Any weak companies should fall off and go bankrupt.

But when you have low interest rates, they can just keep borrowing to keep themselves alive. So companies like AMC and GameStop have taken on a ton of debt. Lot of hedge fund type investors are saying, “These companies don’t deserve to exist. We’re going to short them.” They put on huge short positions and then they get just ambushed by these Reddit [inaudible 00:33:10] It’s kind of in the periphery of the market. I don’t think it’s anything that’s going to create any long-term destabilization in the market. But nothing I’d want to get in investing in, but kind of interesting to watch from afar.

Jim: Every once in a while you’ll see something like this that is just the market finding its way back into, I guess, efficiency and at some point this will change the dynamic between individual investors and hedge funds to some degree. And who knows, maybe it democratizes the markets a little bit. Maybe it changes behavior, but in either case we don’t see it as anything that represents more or less opportunities for longer term investors. It’s just some noise that we have to deal with in the short-term. I would not be very surprised if by the time people were listening to this some of these bubble ups and stock values may have already ameliorated themselves, but that’ll just be a test of how well I can predict the future I guess.

Sam: one of the safer bets you can make in the market right now schemes. They’re not anything that a long-term investor wants to get involved in, but you do make a good point about the power dynamic shifting a little bit in the market with the democratization of trading apps and individuals being able to have unprecedented access to the market between, like I said, opening a Robinhood app on your phone and also you don’t have to trade fees that were barriers for a long time. So there is a lot more individual investors exerting their opinions within the market and I think that’s probably healthy for everybody.

Jim: It’ll be interesting to see obviously their implementing strategies that they think are going to get them their ends, whether their ends are social or economic or whatever. In the past, when the big money’s done that, we’ve called that capitalism and now when the kids are coming in on Reddit and doing it, we’re going to call it manipulation. So we’ll see how it shakes out.

Sam: The funniest thing I find about all this is a lot of the senators are actually going to have hearings about it and whatnot. The two senators that were most vocal about it were Ted Cruz and AOC and you know if those two people

Jim: That’s right.

Sam: But yeah, I think that we just wanted to end on that note for anybody that was interested. Just a little description of what’s going on there, but otherwise just want to thank you for joining us. We will post this up on our website. You can share it if you’d like. We’d love to get it out there for the people to see and we will be back next quarter for you.

Jim: We’re really looking forward to what the next big thing will be then.

Sam: All right. Thanks, Jim.

Disclaimer: The foregoing content reflects the opinions of Penobscot Financial Advisors and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be construed as investment advice or a recommendation regarding the purchase or sale of any security. There’s no