Attention student loan borrowers: Payment forgiveness is ending!

Student loan borrowers are going to have to start making payments on their debts again. Payments will be required starting in October, with interest accrual beginning in September.

This is after 9 consecutive extensions since the pause was put in place under the Trump administration in March 2020. To add to the pain, the US Supreme Court issued a ruling that rendered a major forgiveness initiative from the Biden administration unconstitutional.

Student loan debt, and the resumption of payments is a big deal because:

- It impacts over 27 million people who haven’t been paying over the past three years. (15 million others have continued to make payments, despite the pause).

- Some studies show that 90% of these suspended payments have been going to paying for consumer goods and paying off other debt.

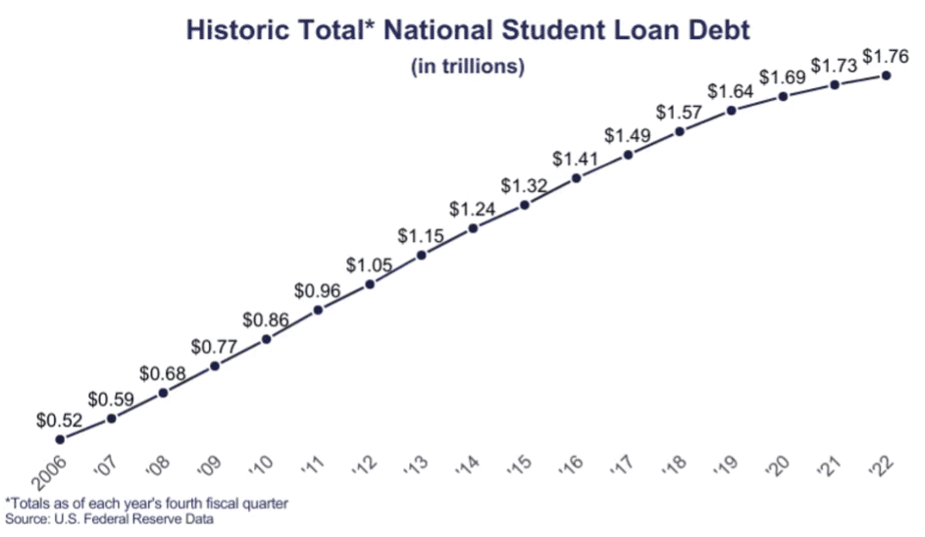

- The average borrower owes $28,950.

- Federal student loans (those that are about to start requiring payment again) account for 92% of student loan debt in existence in this country. The remaining 8% are private loans.

- 15 million people – and everyone who has private loans – have been paying all along and are further ahead… But another 7 million have taken on new debt since the 2020 pause.

The Biden administration had other programs at the ready, including an ‘on-ramp’ program where borrowers wouldn’t face default or credit dings for the first year if they choose not to start payments. Interest WILL accrue during this time, pressing numerous lawmakers to call for a suspension of interest during this period. That’s unlikely for one major reason: That would be tantamount to simply extending the pause for another year – which is exactly what has been decided will NOT occur!

And there’s always the possibility that the legality of even this provision could be challenged and the supreme court could eventually be called upon to rule on it. Long story short, it seems very likely that many people who haven’t been paying student loan payments will be starting to do so this October.

Additionally, and maybe more significantly, another income-driven repayment option is emerging. Income-driven repayments have come about as the result of initiatives put forth by several administrations in the past. The most frequently used plan is called “Revised Pay As You Earn”, or REPAYE. Pay-as-you-earn (PAYE) was signed into law by President Obama in 2012, and the REPAYE revision to that program made for a maximum of 10% of ‘Discretionary Income’ be used to determine payments. Discretionary income, for these purposes, is defined as the amount of income above 150% of the federal poverty level.

One problem with all these income-driven plans is that they can result in ‘negative amortization’, where interest accrued by the balance is higher than the payments – so even though the borrower is making their required payments on the loan, the balance isn’t going down. It’s continuing to increase! REPAYE provides for only 50% of the amount.

A new income-driven repayment plan, called Saving on a Valuable Education (SAVE) is going to improve upon the REPAYE. Starting in July of 2024, borrowers currently paying income driven repayments on the REPAYE plan will move to this new plan. The key features are:

- ‘Discretionary income’ starts at 225% of the poverty level (up from 150%) so less income is included in the payment calculation.

- Instead of 10% of discretionary income, only 5% will be required.

- Any interest will be waived so that the balance cannot increase when the income driven payments are being made (even if income is low enough to make those payments zero). In other words, the problem of ‘negative amortization’ essentially goes away.

There is a lot to unpack when it comes to how to handle student loan debt, both at a societal level and at an individual level. There is plenty of politically charged opinion on the former, and a bunch of complexity on the latter. People vying for loan forgiveness (whether through the Public Service Loan Forgiveness program or regular Income Driven Loan forgiveness) generally aim to keep payments as low as possible, so that there is a balance to forgive. For many, however, the burden of paying for the high cost of higher education in this country is one that needs to be met head-on, with as aggressive a pay down as possible – to limit the amount of interest cost over the long term.

One last thing that isn’t clear: 90% of the money saved through the payment pause was going into the economy to purchase goods and services. The economy is slowing because of unprecedented rate hikes. With all these factors combined determine how much of a downward jolt the economy does on the resumption of student payments? It’s yet to be seen, but it probably won’t be insignificant.