Beware the Social Security Tax Torpedo!

Your quiz of the week: Are Social Security benefits taxable income?

a) Yes

b) No

c) It depends

If you’re at all familiar with federal programs and taxation, I hope you chose c without any hesitation. Tax issues are never so cut-and-dried that they can be answered with a simple ‘yes’ or ‘no’, which is somewhat fortuitous, because this would be a very short blog post if they were!

Federal taxation of Social Security benefits depends on a number called “Provisional Income.” This is different from your Taxable Income or your Adjusted Gross Income. It includes:

- All income that would normally be taxable (wages, interest, business income, capital gains, etc…)

- Some income that is not taxable (tax-free municipal bond interest)

- HALF of your Social Security benefit

EXAMPLE: Rick and Mary have $35,000 in pension, take $6,000 from an IRA, have investments that generate $1,500 in capital gains and $500 in interest income, as well as $1,000 of tax-free income from municipal bonds. They also receive $38,000 total from Social Security. Altogether, their Provisional Income is the total of the non-Social Security income sources ($44,000) PLUS half of their combined Social Security benefits ($38,000 / 2 = $19,000). $44,000 + $19,000 = $63,000 in Provisional Income.

Once we figure out the Provisional Income, we compare this amount to two separate thresholds: These are $25,000 and $34,000 for single filers and $32,000 and $44,000 for married filers. Next, there are three tests to determine how much of the Social Security income will be included as Taxable Income:

- TEST ONE: 85% of Social Security Benefits.

- TEST TWO: 50% of benefits plus 85% of Provisional Income beyond second threshold amount.

- TEST THREE: 50% of Provisional Income beyond first threshold plus 35% of Provisional Income beyond the second threshold.

The lowest of these three numbers is the amount of Social Security subject to taxation. For simplicity’s sake, this results in the following treatment.

- Taxpayers whose Provisional Income falls below the first threshold don’t pay tax on their Social Security benefits.

- Taxpayers whose Provisional Income falls between the two thresholds pay taxes on UP TO 50% of their Social Security benefits.

- Taxpayers whose Provisional Income falls above the second threshold pay taxes on up to 85% of their Social Security benefits.

This means that every Social Security recipient gets at least SOME of their benefit federal income tax-free. It also means that people who most rely on their Social Security benefits (those whose Provisional Income falls below the lower thresholds) don’t have to pay any income tax on these benefits.

This means that every Social Security recipient gets at least SOME of their benefit federal income tax-free. It also means that people who most rely on their Social Security benefits (those whose Provisional Income falls below the lower thresholds) don’t have to pay any income tax on these benefits.

Most states (including Maine) don’t tax Social Security benefits, but there are 13 that do. They are Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont and West Virginia.

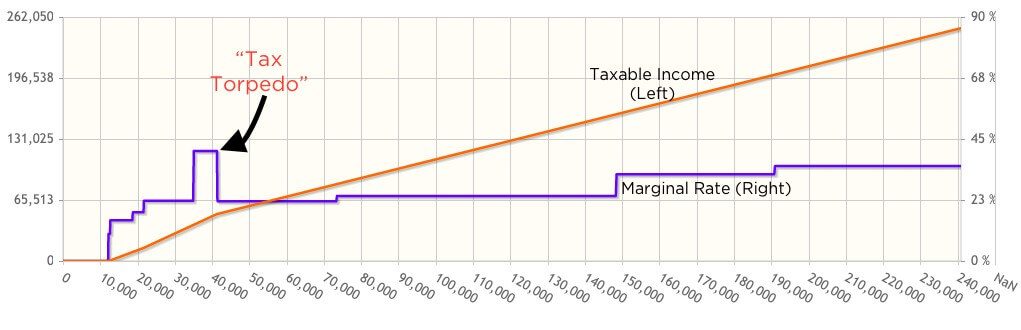

This progression of more Social Security benefits becoming taxable as income increases creates some interesting planning conundrums when determining how to fund needs while collecting Social Security. This can cause some unexpected increases in taxation on additional income.

EXAMPLE: Rick and Mary from the example above want to fund a vacation by taking $4,000 more out of their IRA this year. Their income puts them in the 12% federal tax bracket, so they figure the distribution should cost them ($4,000 x .12 =) $480 in additional federal income. But, this additional $4,000 will also increase their Provisional Income, thus increasing the amount of their Social Security benefits that will be taxable. Since they’re beyond the second threshold number, they will increase their taxable Social Security benefits by 85% of this distribution, or ($4,000 x .85 =) $3,400. At their current 12% federal income tax bracket, they will incur an additional ($3,400 x .12 =) $408. This brings the tax impact of the additional IRA distribution to ($480 + $408 =) $888, for an effective tax bracket of not 12% but ($888 / $4,000 -) 22.2%!

The bump in the marginal tax rate that Rick and Mary experienced is something we refer to as the “Tax Torpedo”. It only occurs in the space between the lowest Provisional Income threshold levels (below which there is no taxation on Social Security) and the point where 85% of Social Security is already being taxed (after which no more impact occurs).

When in this “Tax Torpedo” zone, it may make sense to pay for additional expenses from things that won’t create additional Provisional Income. One potential solution is to take from regular savings, if available. In our example above, if Rick and Mary have a Roth IRA, they could take the vacation money from that account. Roth IRA distributions do not impact Provisional Income, making them a very attractive tool as part of a retirement portfolio. They could also sell out of an investment outside of their retirement plans, even if it means realizing a capital gain on the sale. In the case of Rick and Mary, their income puts them solidly in the 12% federal income tax bracket and at that bracket, the capital gains tax rate is zero. Sure, they’d still pay on the extra amount of income caused by the capital gains, but the amount would be almost certainly lower than the Torpedo impact of an IRA distribution because they almost certainly have some ‘cost basis’ in the position they sell, reducing the taxable amount. (This strategy is sometimes called “Gain Harvesting”.

When in this “Tax Torpedo” zone, it may make sense to pay for additional expenses from things that won’t create additional Provisional Income. One potential solution is to take from regular savings, if available. In our example above, if Rick and Mary have a Roth IRA, they could take the vacation money from that account. Roth IRA distributions do not impact Provisional Income, making them a very attractive tool as part of a retirement portfolio. They could also sell out of an investment outside of their retirement plans, even if it means realizing a capital gain on the sale. In the case of Rick and Mary, their income puts them solidly in the 12% federal income tax bracket and at that bracket, the capital gains tax rate is zero. Sure, they’d still pay on the extra amount of income caused by the capital gains, but the amount would be almost certainly lower than the Torpedo impact of an IRA distribution because they almost certainly have some ‘cost basis’ in the position they sell, reducing the taxable amount. (This strategy is sometimes called “Gain Harvesting”.

A beloved mentor of mine was known for really corny jokes. One of them had the punchline “Damn the poor Titos. Full steed ahead!”. Sadly, I only remember the punchline, so I’ll spend some time reconstructing the joke later. Meanwhile, YOU might want to spend time constructing your portfolio to be ‘Torpedo-resistant.’ Setting up a full range of account types, including tax-deferred, tax-free and taxable assets is a great way to start.