The ‘Boring’ I-Bond: It’s not so boring right now.

Investing in bonds, whether to diversify a portfolio, to produce reliable income, or to simply hold onto some money for a ‘rainy day’, has been challenging over the past few years. Interest rates, which started to look slightly more competitive in 2018 and 2019 returned to even lower levels in 2020 and haven’t markedly recovered. Add recent inflation to the mix, and the real rate of return on most bonds is negative; money you set aside for that rainy day might not buy as much as it would have when you socked it away.

One response to this challenging conundrum has been for investors to willingly take risks by purchasing lower quality bonds that carry higher probability of default, to lock in a slightly better rate of return, pushing up prices and lowering expected returns on these assets. Other investors have steered away from bonds entirely, relying on stocks and, you guessed it, bidding up prices and lowering potential returns from these more volatile investments. The acronym ‘TINA’ (There Is No Alternative) has been thrown around in this market environment – investors focused on inflation risk are buying up stocks at what some would consider lofty prices, simply because they aren’t able to find other investments that can outpace the rate of inflation.

Right now, though, there IS a bond that provides a solid 7.12% annualized rate of return, tax-deferred growth, and whose principal value is backed by the full faith and credit of the US Government. If you’re willing to jump through some relatively easy hoops, this could be the mixture of yield and safety you’ve been waiting for: The US Savings Bond known as the i-Bond.

Series I-Bonds: The Basics

If you grew up when I did, you probably accumulated a stack of series EE-bonds during your childhood as the result of gifts from grandparents, aunts and uncles, and school savings programs. Back in 1998, a new type of savings bond, the I-Bond came into being.

Series I-Bonds work differently from the series EE-Bonds in a few ways, most notably in how interest is calculated. There is a ‘Composite Rate’ which is the sum of a ‘Fixed Rate’ and an ‘Inflation Rate’ and is released on November 1 and May 1 of each year. Series I-Bonds issued during that period will earn the announced annualized composite rate for a six-month period, after which they renew every six months at the newly announced composite rate.

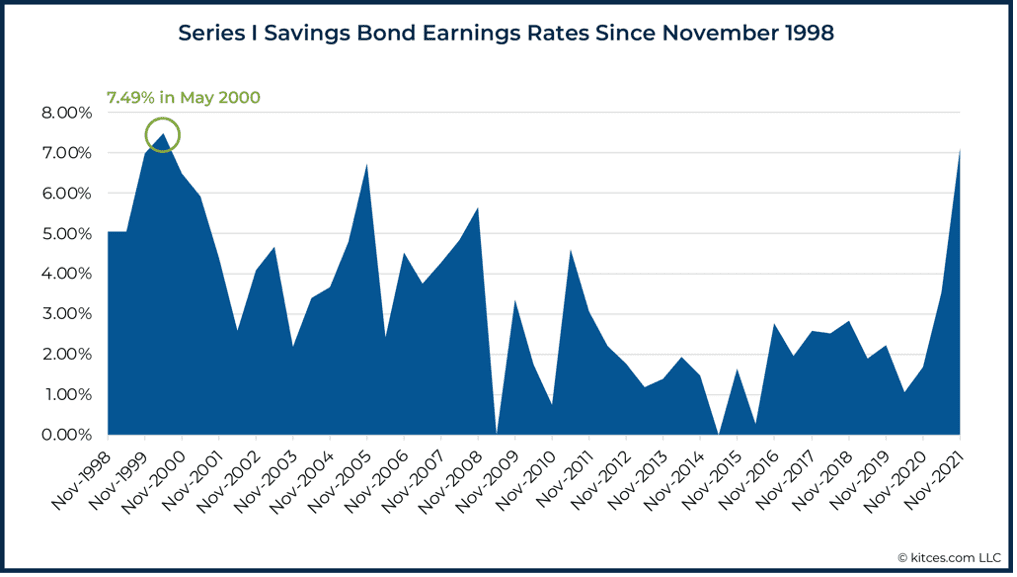

Right now, the fixed rate on I-bonds is 0%. Not that exciting. Probably around the same rate you’re getting on your bank account. However, for I-bonds issued before May 1, 2022, the inflation rate in effect is 7.12%. Since the composite rate on I-bonds is the sum of the fixed and inflation rates, your compound annual rate is 0% + 7.12% = 7.12%! This rate is the highest we’ve seen since May of 2000!

Unlike most corporate bonds, I-Bonds can be redeemed prior to maturity at ‘face value’ – meaning that if interest rates go up, this won’t impair the value of the bond in the open market. I-Bonds have a 20-year maturity plus a 10-year extension (essentially, they have a 30-year maturity), after which they no longer are credited with interest.

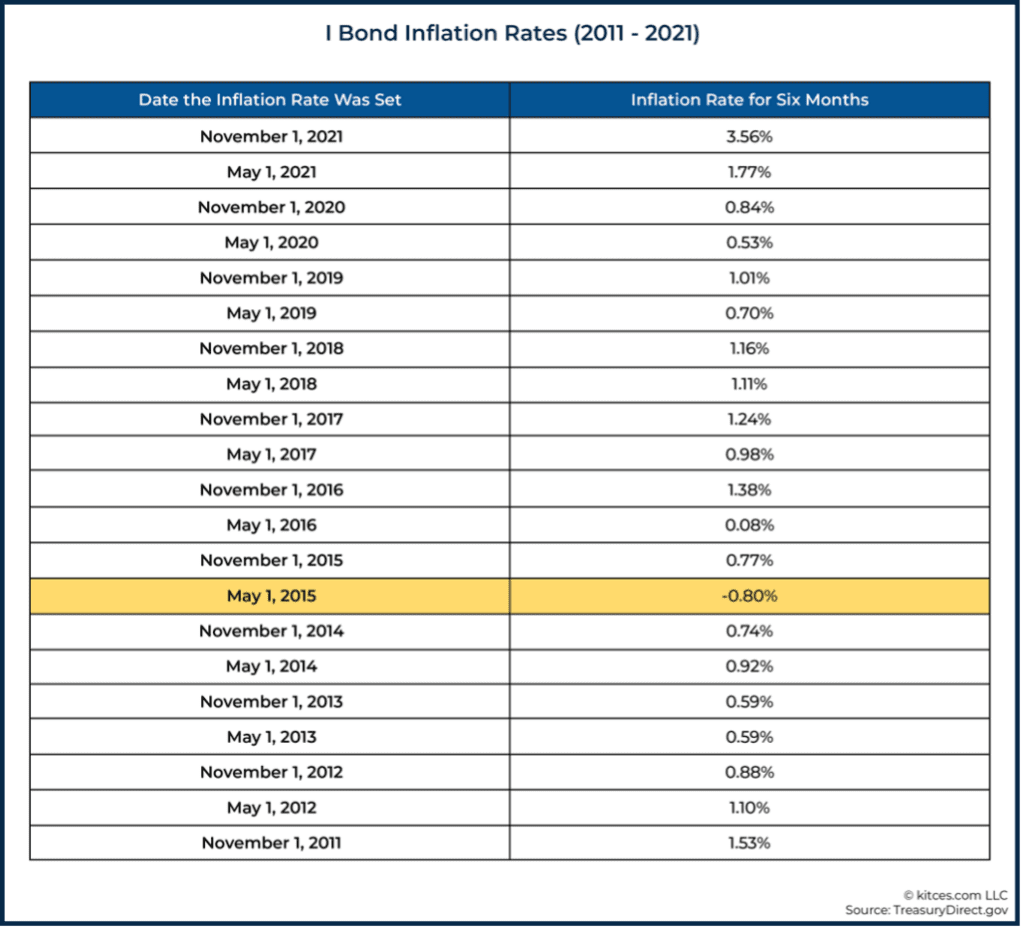

Also, the composite rate of interest on I-Bonds will never go below zero, which is important, since at the current fixed rate of zero, a negative inflation release would otherwise turn the composite rate negative. Looking at historical rates below, if we had another May 2015 reading, the composite rate would not go below zero even if the fixed + inflation rates tallied to a negative number.

Interest on I-Bonds is federal-tax-deferred and completely exempt from state and local taxes. In fact, if proceeds from an I-Bond are used to pay for qualifying education expenses, the interest is also exempt from federal taxes (i.e. Tax-Free!)

Sounds too good to be true… What’s the catch??

Before you back up the truck and empty out your bank account, let’s make sure we look at some of the restrictions around I-Bonds.

#1: They are illiquid for one year. Unless you live in a Federally declared disaster area.

#2: If you cash them in within 5 years of purchase, you forfeit the prior three months’ worth of interest. After 5 years, you can redeem your I-Bonds at any time without forfeiture of any interest.

#3: You can only purchase $10,000 per year online at www.treasurydirect.gov, per Social Security number

The initial one-year liquidity restriction renders I-Bonds inappropriate for someone who may need the money sooner. Short-term contingency funds should be available, either in outside bank accounts or in savings bonds that have already met the one-year minimum holding. Also, while you know your rate for the first six months, you do not know up front what the composite rate will be for the second six months before you can cash in the I-Bonds.

While the $10,000 per year per Social Security number puts a substantial limit on how much you can benefit from these rates, there are ways of maxing out your ability if you act soon. A purchase in 2021 with a subsequent purchase prior to May 1, 2022 would double the amount of I-Bonds you own making the 7.12%. If you have a spouse, both of you can purchase $10,000 worth of I-Bonds per year. If you have children, grandchildren, nieces, nephews, friends – you can purchase up to $10,000 per year for each of them. If you have a trust or estate or even a corporate entity with its own tax ID, each of those can purchase $10,000 per year. And when you file your taxes, you can get your refund (up to $5,000 per return) in I-Bonds, above and beyond the $10,000 annual limit. Planning can yield benefits.

Example: Keith and Nicole have money they’ll be needing for tuition payments in 2023 when their daughter LeeAnn starts college. They can each purchase $10,000 in I-Bonds before 12/31/2021 and once again in January 2022. Additionally, they can purchase $10,000 for LeeAnn during both periods and, since Nicole has an LLC with its own tax ID and they have a family trust with its own tax ID, they can put $10,000 from each of those entities for both years. Additionally, when they file their tax returns in 2022, they can opt for up to $5,000 of their refund to be issued as an I-Bond – or, if they file separate returns, they can both get the additional $5,000. They could conceivably have over $100,000 working hard at the 7.12% rate.

Even though you won’t know what the renewal rate will be during the second half of the first year when you will be compelled to hold these I-Bonds, the yield can still be compelling, even if rates take a big turn downward.

Example: Keith and Nicole have purchased I-Bonds that, given the 7.12% annualized rate, will provide them with over 3.5% interest over the first six months. Even in a ‘worst case’ scenario where the consolidated rate announced May 1, 2022 is ZERO (something they see as improbable), they are still looking at a fully guaranteed rate of over 3.5% – unreduced for early liquidation since the three months of forfeited interest would have been zero. They’ve been looking at 1-year FDIC-insured CD returns at their bank and found they return only about 0.5% and are fully taxable, even for college expenses.

I-Bonds are too high-yielding and safe right now to be ignored. People with money to park who want to diversify their inflation risk management should absolutely consider them!