The SS Hedge

Faced with uncertainty in markets and the economy, asset managers, when possible try to hedge away unwanted risk. They… uh, WE… focus on areas where we can add value through smart decisions; using all of the analytical tools we have at our side. Sure, we get paid to take risk, but we want to be smart about it.

One area that seems to get passed over more than it should is Social Security income planning. Given that some of the more esoteric Social Security strategies are, or soon will be, extinct (Google the terms ‘File-and-Suspend’ or ‘ Restricted Application’), the remaining strategy decision comes down to a relatively simple question of whether benefits should be taken currently or delayed.

As simple as it sounds, this is actually a pretty complex decision, especially in the case of married couples. For single filers, as a general rule, if you think you will live long enough to make up for the foregone year(s) of Social Security by starting later and getting higher benefits, the delay may make sense[1].

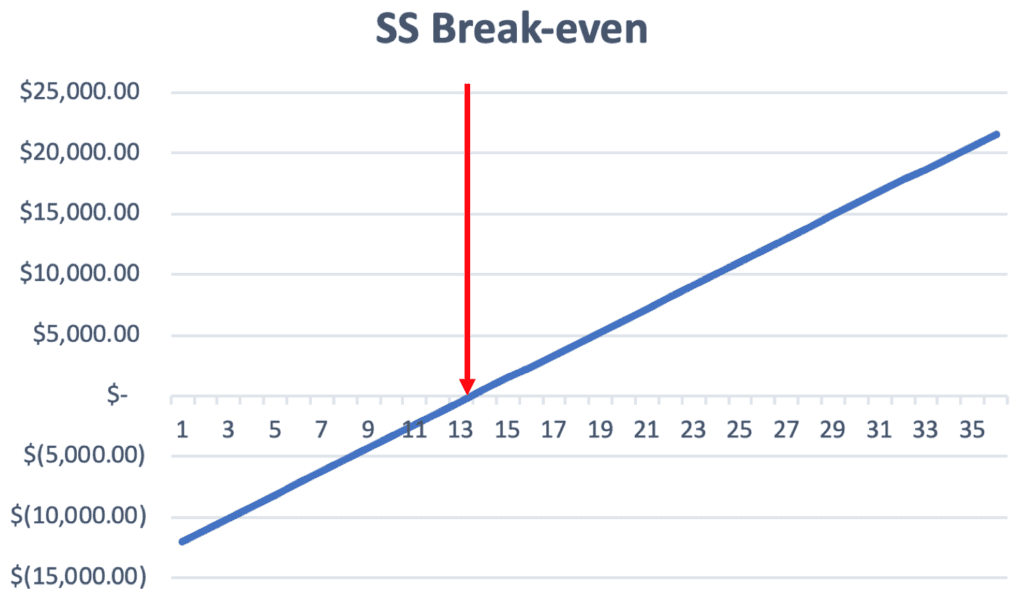

So, how long does it actually take to make up the difference? If, by delaying benefits by one year, you get an 8 percent increase to your benefits (the standard amount for delaying past your Full Retirement Age), it should take about 13 years of taking the higher amount to close the gap created by the delay.

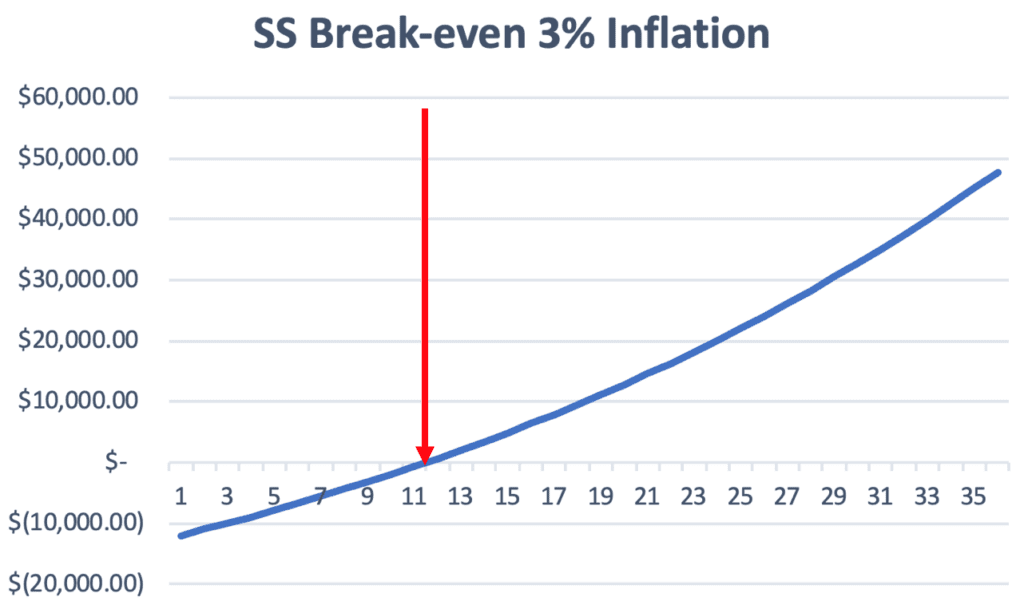

But wait – if benefits are increasing each year, the annual increase will be more substantial to the higher benefit. Assuming a 3 percent rate of inflation, the ‘breakeven’ occurs about 2 years earlier, or 11 years out. If inflation were higher, the breakeven would occur even earlier. Higher inflation makes delaying benefits a more attractive option.

But wait – if benefits are increasing each year, the annual increase will be more substantial to the higher benefit. Assuming a 3 percent rate of inflation, the ‘breakeven’ occurs about 2 years earlier, or 11 years out. If inflation were higher, the breakeven would occur even earlier. Higher inflation makes delaying benefits a more attractive option.

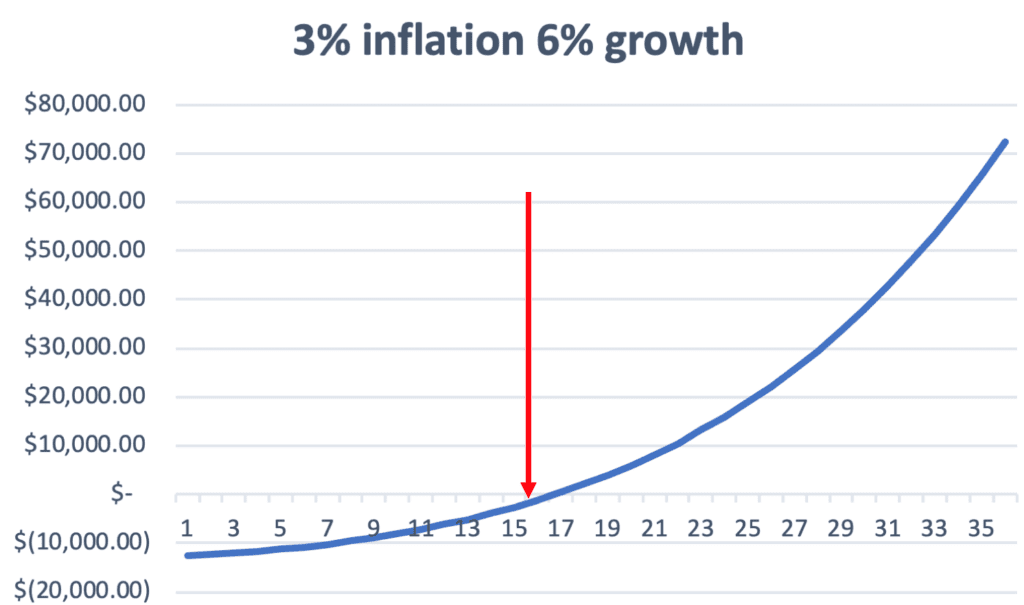

That said, including inflation assumptions only addresses one side of the delay issue. Another side that should be considered is the fact that, by delaying benefits, there is an opportunity cost created by either having to take money out of assets (since SS is being delayed) or not having extra income to invest. This ‘cost’ is the amount that investments would have grown by had they not been removed by the delay decision. This creates a ‘drag’ on being able to reach the break-even. Furthering our model from before, adding a 6% investment growth rate (that’s the ‘opportunity cost’), pushes the break-even period out to 17 years. Higher investment returns hurt more, and lower investment returns are better in the case of a delay decision.

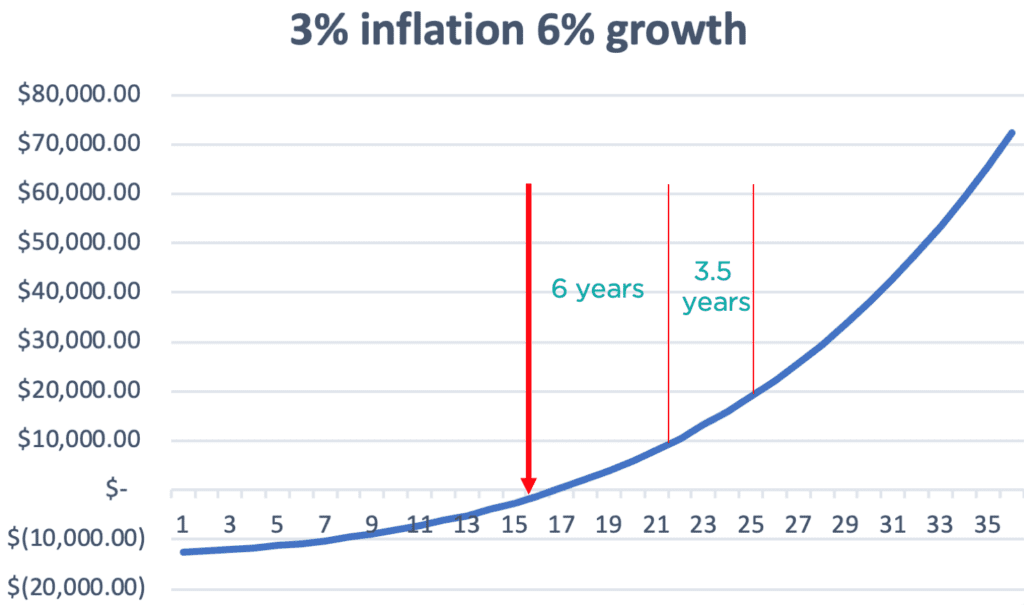

Although the inclusion of investment opportunity cost delays the breakeven on a delay strategy, it also increases the benefit of delaying once someone does cross the break-even age. In a case where someone foregoes a $1,000 monthly benefit to start a higher benefit (say, $1,080) the following year, they begin the second year $12,000 ‘in the hole’ and that’s the delay penalty they need to make up. Continuing the last example, if we assume 6 percent investment opportunity cost, it takes about 17 years to make up the $12,000. However, once it’s made up, it only takes another 6 years for the recipient to be AHEAD by $12,000… and around 3.5 years later, the recipient is up another $12,000! In other words, longevity can substantially magnify the benefits of the delay decision.

Here is the point of all this: When we are planning retirement and needing to live off of a base of assets, we have a few major challenges (risks) that we need to consider:

Here is the point of all this: When we are planning retirement and needing to live off of a base of assets, we have a few major challenges (risks) that we need to consider:

- Higher than expected inflation

- Lower than expected investment returns

- Higher than expected longevity

Those three risks to an investment portfolio are exactly the three things that actually work to improve outcomes under a Social Security delay strategy!

The decision on when to take Social Security is one that deserves close attention and analysis. Well-thought-out strategies will reduce the risk that you run out of money during your life. Take the time to get it right, and make an asset manager happy!

[1] https://personal.vanguard.com/us/insights/retirement/plan-for-a-long-retirement-tool?lang=en features a great tool for estimating the probability you will live past your breakeven point – or any other hurdle!